Arm Holdings Limited (“Arm”) has on the 21st of Aug 2023, announced that it has publicly filed a registration statement on Form F-1 with the U.S. Securities and Exchange Commission (“SEC”) relating to the proposed initial public offering of American depositary shares (“ADS”) representing its ordinary shares.

This will represent one of the biggest initial public offerings we have this year with Softbank looking to raise up to $4.87 billion at the top range, offering 95.5 million American depository shares for between $47 to $51 a piece.

The proposed range would value the company at between $48b to $52b, which is higher than the failed $40 billion deal Softbank was trying to sell to Nvidia Corp last year because of anti-trust concerns.

Should investors get in and buy this IPO? Let’s deep dive for its fundamentals to find out.

Business Model

Arm is defining the future of computing.

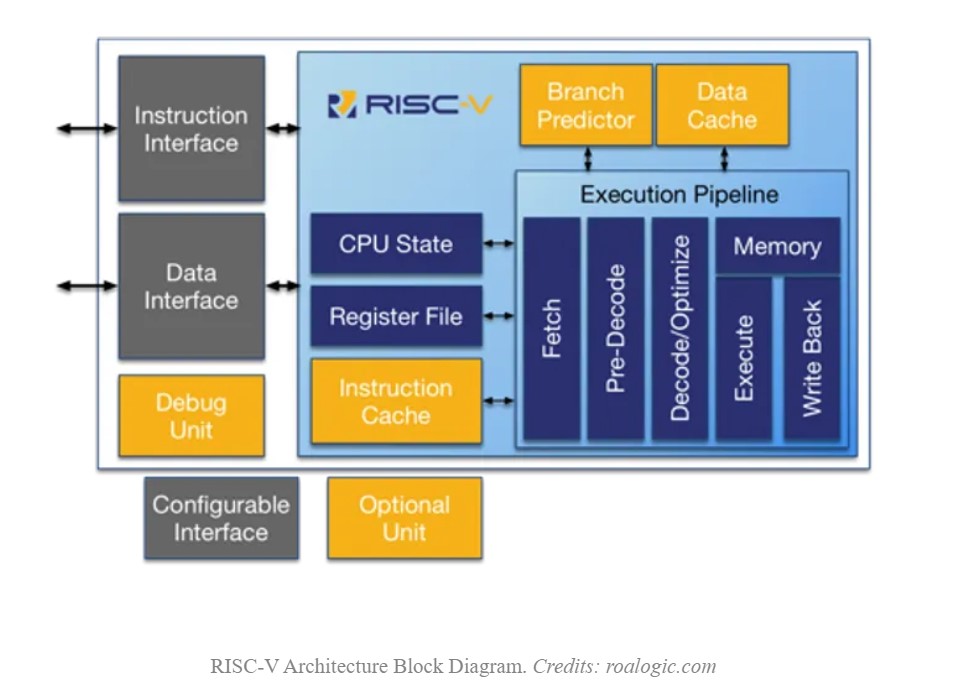

Semi-conductor technology has become one of the world’s most critical resources, as it enables all electronic devices today. At the heart of these devices is the central processing unit (“CPU”) – and ARM is the industry leader of CPUs.

The company architects, develops, and licences high performance, low-cost, and energy-efficient CPU products, on which many of the world’s leading semi-conductor companies and OEMs rely to develop their products.

It is estimated that approximately 70% of the world’s population uses Arm-based products.

The company earns its revenue by licensing its portfolio of ARM products, rather than licensing a single individual CPU product. This way, the company made it more compelling for businesses to utilize more ARM products, further broadening and penetrating the existing customer base. This also helps to increase the recurring royalties paid to them whenever businesses use them.

Some fun facts information: approximately 46% of the royalty revenue for the fiscal year ended 31 March 2023 came from products which were released between 1990 – 2012.

Financials and Fundamentals

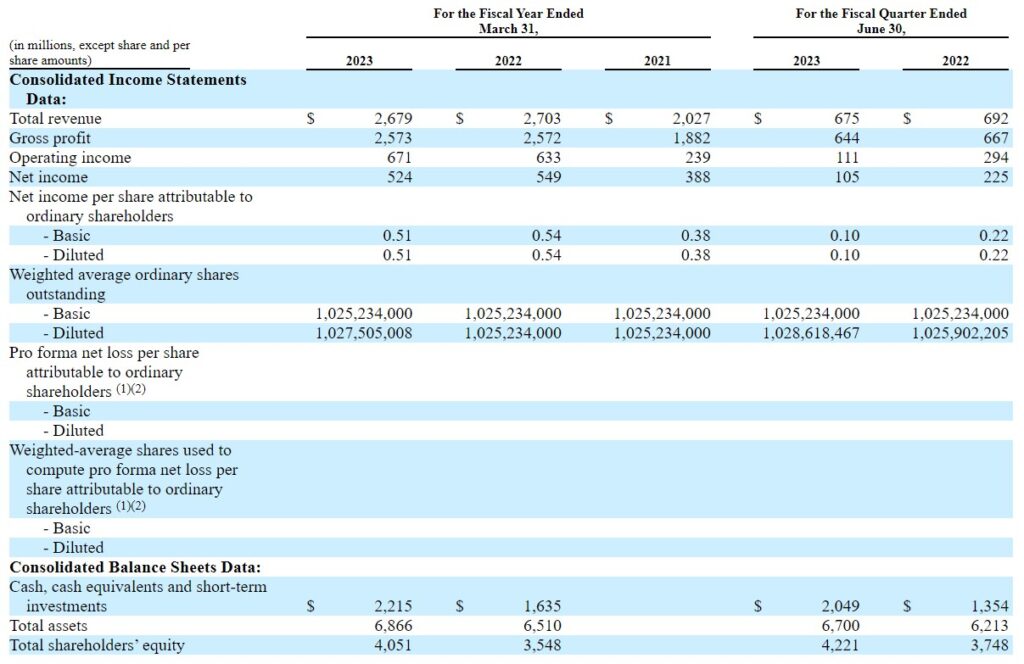

A quick glance over its financials shows that the company has been generating a steady stream of increase in revenue from 2021 to 2023 for the past three years, increasing from $2.02 billion to $2.68 billion.

That represents a total CAGR of roughly about 9.88% per annum across the three years, which is very decent for a company of that size. However, the past one year from 2022 to 2023 has been rather flat, so there’s some concerns if the company is able to continue its trajectory growth over the next few years.

Management has estimated that their total addressable market (“TAM”) is approximately $202.5 billion in 2022 and is forecasted to grow at a 6.8% compound annual growth rate (“CAGR”) to approximately $246.6 billion by the end of the calendar year ending December 31, 2025 while the aggregate value of chips containing Arm technology was approximately $98.9 billion in the calendar year ended December 31, 2022, so that represents a 48.9% market share and there’s obviously some organic growth projections built in there.

Gross profit margin as a percentage of the total revenue was 96% while operating income margin was 25%.

All three segments – Gross profit margin, operating income margin and net income margin have been stable across the years in comparison against the total revenue.

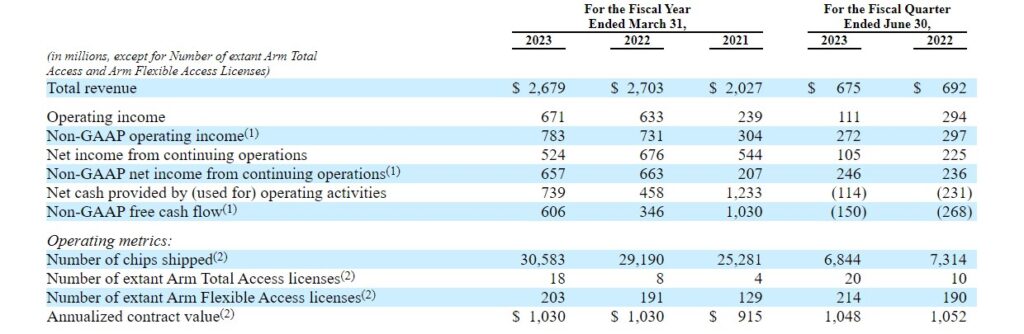

Cashflow from operations and free cash flow are fluctuating over the year due to joint investment due to equity, working capital and capex spending movement.

For instance, while the company earns lesser revenue in 2021 relative to 2022 and 2023, it generates a higher cash flow from operations and free cash flow.

Capex sending has trended at about 8-9% of its operating cash flow over the years.

Risk Factors

There are a few risks that I thought is worth highlighting.

First, there is a notable portion of concentrated customer risk.

A significant portion of the total revenue is generated from a limited number of key customers. In particular, the top 5 customers collectively accounted for approximately 57% of the total revenue for the fiscal year ending March 2023. The largest customer, which is ARM China, accounted for approximately 24% of the total revenue.

Second, there is also stiff competition risk.

Many of the customers are also major supporters of RISC-V related technologies, which operates as an open-source instruction set architecture (ISA) as opposed to ARM which operates as a proprietary ISA.

The ongoing distinct advantages between both technologies revolve around the different ISAs they embody, each offering and catering to the computing needs of the businesses.

Third, other than the concentrated risk coming in from top customers highlighted in point 1, there is also a concentrated risk coming in from geographical area. For the fiscal year ending 31 March 2023, revenues from the PRC accounted for approximately 25% of the total revenue, including the relationship with ARM China.

Furthermore, PRC has been a significant source of semi-conductor industry growth lever, and with the tension running high between USA and China for a number of years now, there might be implications over how political conflict might come in to ban the usage of these technologies.

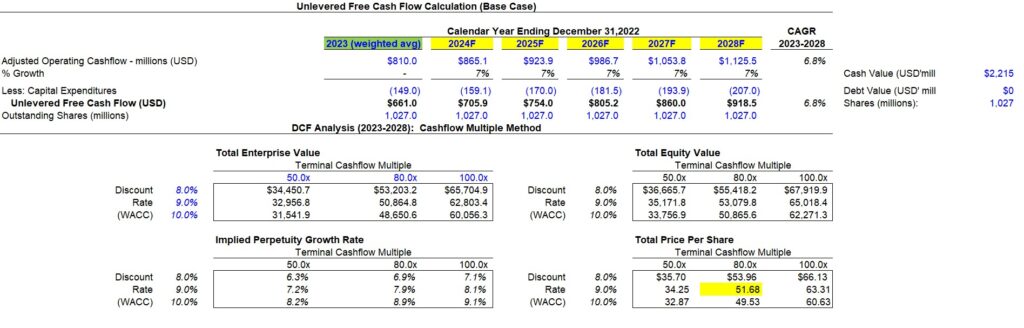

Company Valuation – DCF

It is not easy to do a company valuation using a DCF method when all we’ve got is the past 3 years history in the prospectus. Furthermore, the technology landscape is moving fast, so it will not be easy to project future growth as well.

For the purpose of this exercise, we will simply use the weighted average free cash flow for the past three years, and then we will assume a growth rate of 6.8% in the next 5 years based on the projections that management has guided in their TAM projection outlook.

In late 2020, Softbank tried to offload ARM to Nvidia for $40b, a move which had it gone through would have been the biggest chip deal in the history. Unfortunately, it didn’t go through beacuse of anti-trust concerns.

Still, if we calculate back as to how much Nvidia was willing to pay for $40b valuation – at a revenue of $2b and EPS of $0.38, that would have represented a Price to Sales multiple of 20x and Price to Earnings multiple of 105x. That is very high considering for a company that has a projected modest single digit growth going forward.

Of course, with the Nvidia merger, there could be synergy in the making and both businesses could have flourished even more, but we’ll never know now that the deal is off.

For this exercise, I will put the three-case multiple scenarios to be at 50x, 80x, and 100x.

As you can see, with just a modest growth expectation of 6.8% over the next 5 years, and fetching over 80x multiples, the intrinsic value of the company is barely at $51.68. The company is offering between $47-$51 a piece in the IPO.

In other words, they are pricing in at the higher end of the spectrum at about 80x multiples based on 2023 earnings.

With just a modest growth and all the risks that it represents, I think this is a miss in my opinion.

Any adverse effects surrounding China-US tension can easily halve the valuation, especially if further growth is not justified either.

If you have not followed my social channels, you may want to do so as I frequently post ideas and thoughts in those channels so if you are interested, you may follow me at my Facebook, Instagram, Twitter or Threads profile here.