Alibaba Group Holding (NYSE: BABA) just reported earnings for the quarter ended 30 June 2023.

Let us take a look at its reported financial results in a nutshell:

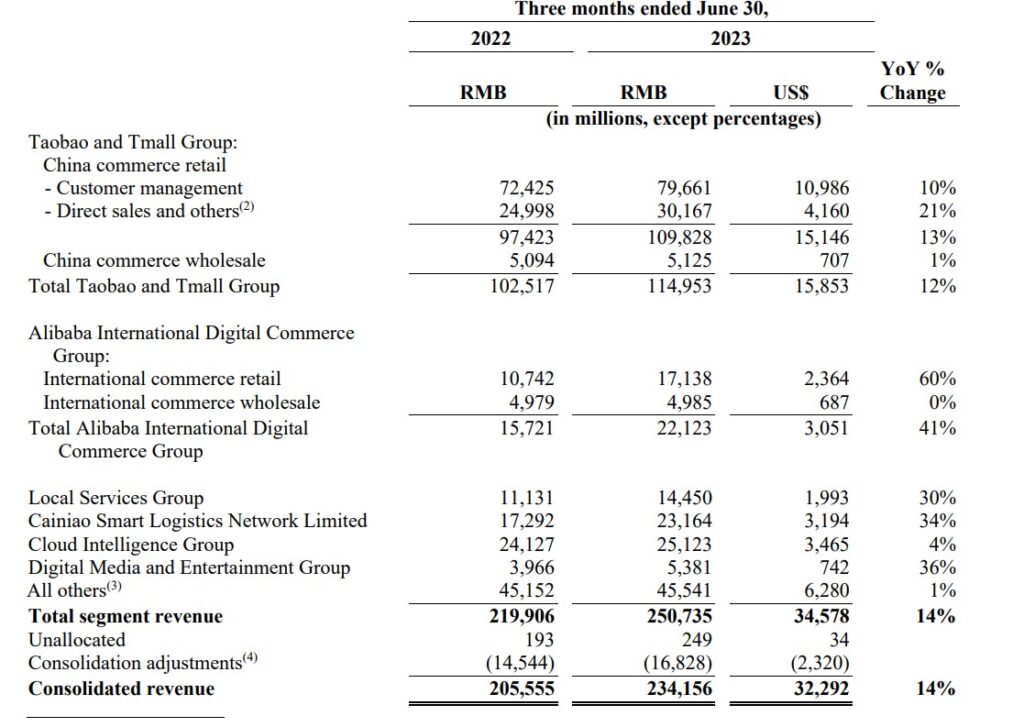

- Revenue was up 14% year on year to RMB 234,156 million (USD 32,292 million).

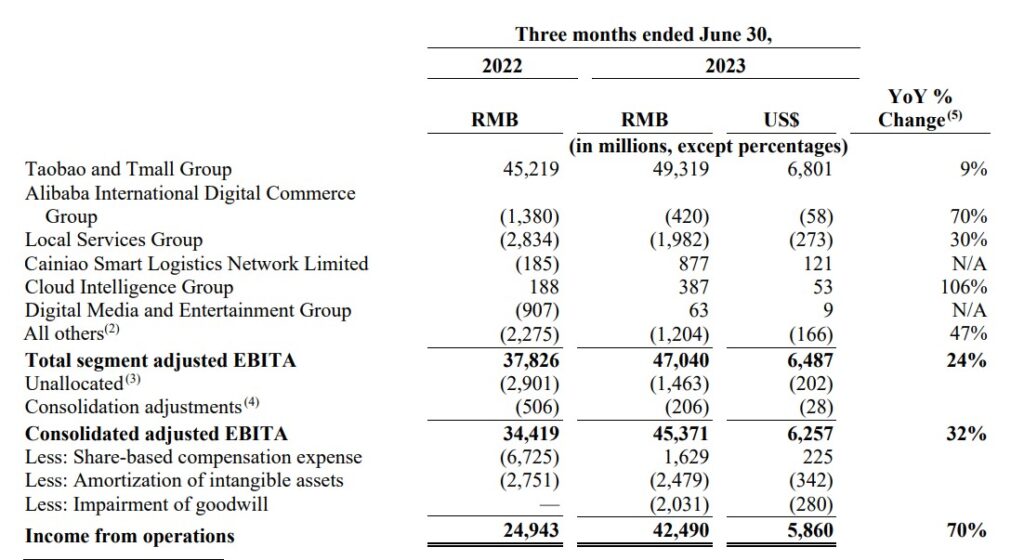

- Income from Operations was up 70% year on year to RMB 42,290 million (USD 5,860 million). This was due to the one-off reversal of share-based compensation expense of RMB 6,901 million (USD 962 million) which helped to boost. Without this, income from operations would still have been up but lesser by 43% year on year.

- Net Income attributable to ordinary shareholders was RMB 34,332 million (USD 4,735 million).

- Non-GAAP net income was up 48% year on year to RMB 44,922 million (USD 6,195 million)

- Operating Cashflow was up 34% year on year to RMB 45,306 million (USD 6,248 million). Free Cash Flow was up 76% year on year to RMB 39,089 million (USD 5,391 million).

Overall, as we expected, financial results turn out better as compared to the previous year as the company continues to reorganize and prioritise core businesses.

From each business segment point of view, it is also reporting good increase year over year.

Taobao China commerce managed to increase 6.5% Daily Active User increase year on year while topline revenue increased by 12% to RMB 114,953 million (USD 15,853 million).

International commerce was the biggest surprise as it registered a 60% increase year on year to RMB 17,138 million (USD 2,364 million) due to strong investment that paid off over the years.

Cainiao logistics segment also registered healthy growth over 34% year on year primarily due to increase in revenue from international fulfilment solution services and domestic consumer logistics services.

Cloud growth took a stall at it only grew by 4% year on year as competition intensified across the board.

Digital media also impressed by registering strong growth of 36% year on year primarily driven by growth in online entertainment business and strong recovery of offline entertainment business.

All other segments of the business such as Alibaba Health, Freshippo, and Fliggy remained stable year on year.

It was not just the revenue that impressed this quarter, but many segments also performed well on bottom line EBITA expectations across the board.

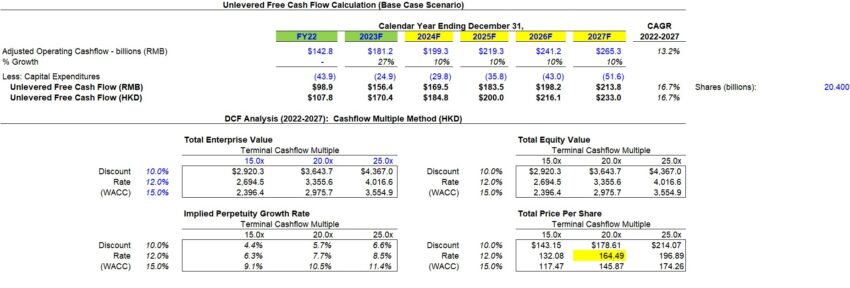

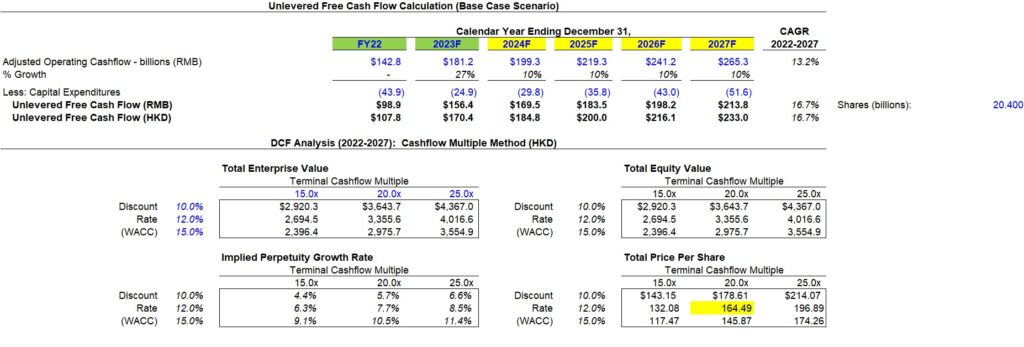

Valuation: Discounted Cash Flow Methodology

I will refresh my DCF valuation table based on this latest quarterly result to see if there’s any further meat on the table.

It is important to note that the company has repurchased share buyback which was great for the ordinary shareholders because there was a reduction of 136.8 million shares from the last quarter, and as of 30 Jun 2023, the company has 20.4 billion ordinary shares (ending last year was 21.4 billion ordinary shares).

I have annualised this quarter operating cashflow, and together with the reduction in capex spending (past investment have started to bear fruits), projected free cash flow for the year is in the range of RMB 156 billion or RMB 39 billion per quarter.

We then project a 10% growth from this rate all the way to 2027, and we expect both the Chinese and International commerce to continue to do well under the circumstances of recovery in the economy.

A cashflow multiple of 20x was then applied, this is higher than the current 24x earnings multiple they are trading, and with expansion multiple, this may well grow as well.

We came up to an intrinsic value of HKD 164.49 or around USD 168 per ADS.

This was up from the previous valuation of HKD 117 when we were expecting a growth in 2023 of only 10% instead of the 27%. We’ll continue to monitor and see if the growth can be materialised further with the plan to break the division in the upcoming next few quarters.