Sea Ltd made a few sensational headlines recently with its drastic cost cutting measures which puts the company back into profitability from last quarter.

We are not just talking about headcount hiring freeze or salary increment pause. We are also hearing news from inside that they were removing all benefits which were provided previously to staff such as pantry benefits and massage & game room. But what really stole the headline was its drastic move to change its toilet paper from a 2-ply to 1-ply and this is where management really meant business.

You can read that article here if you are interested.

In this article, we’ll look at its Q1 FY2023 performance and we compare it against last year during the same period, and we will also compare it against Q4 of last year.

But before that, let’s look at the summary for this Q1 FY2023:

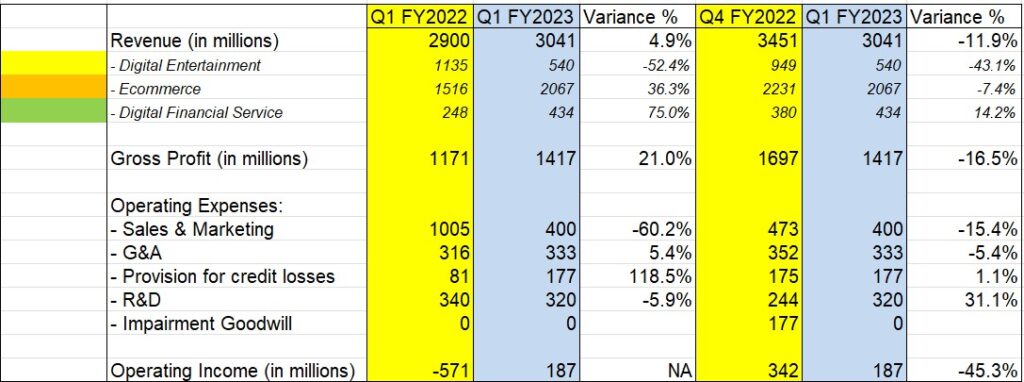

- Total GAAP Revenue was $3.04b – up ~4.9% year on year.

- Total Gross Profit was $1.4b – up ~21% year on year.

- Total Operating Income was $187m – the second consecutive profitable quarter.

- Total Adjusted EBITDA was $507m, which was an improvement from the previous year loss of -$(510m).

While we notably see an improvement year on year, some quarter-on-quarter relative performance are due for concerns that may be related to seasonality, but others may be permanent in nature.

- HUGE concerns over Garena Digital Entertainment performance in this quarter as revenue dropped from $1.1b in Q1 last year to $950m in Q4 to $540m in Q1 FY2023 now. The decline in active and paying users as well as no relative new games coming up are hitting them really hard for this. From what used to be a cash cow machine in the past has now dwindled down to back-up substitute. In fact, I reckon the Digital Financial Service might even take them out from second position from next quarter.

- Shopee E-commerce segments are doing very well. Revenue has picked up 36% this quarter YoY to close at over $2b, which was a shy away from the peak they did last Q4 quarter. Seasonality could also play a part here so we should still see stronger performance to come in the next few quarters.

- Seamoney Digital Financial Services segment are still picking up and it is performing better in this quarter than it did back in Q4, showing this might have more room for further growth.

- Provision for credit loss is going to increase in tandem with Seamoney growth as they now have to fully provision for bad debt loss that they are not going to recover.

- R&D has also picked up again in this quarter with a spending of over $320m, and I suspect this might be for the upcoming new games they intend to launch to support their game segments.

1-Ply Toilet Valuation

Let’s see how much Sea’s valuation is now.

I’ve actually downgraded their intrinsic valuation due to the fact that I’ve changed the multiple model for their e-commerce segment from Sales to EBITDA multiple since i.) they are primarily profitable now and ii.) it doesn’t look like they will scale aggressively anymore into other markets

- Net cash has now increased slightly to $7.2b.

- Digital entertainment valuation continued to plummet down as this has now worth only at $12.4 based on the 8x EBITDA multiple.

- E-commerce was the biggest change here in terms of how I modelled it. With this segment profitable now, we can now benchmark this to the same multiple as the other e-commerce is doing (such as Baba, Amazon, MELI, etc). This segment is now the new cash cow and management is likely going to be very careful not to over-scale in markets they are not confident in.

- SeaMoney valuation has increased as a result of their expansion growth and will continue to scale with high growth.

This brings the overall intrinsic value for Sea Ltd at around $81. With not much margin of safety currently at today’s market price, I’ll likely stay sidelines and continue to monitor the situation from here.