Financial Independence has been an agenda movement devoted to a systematic programming of financial prudence – which includes increasing income, extreme savings, and higher investment pots.

The 1992 best-selling book Your Money or Your Life by Vicky Robin is thought provoking for many salaried workers because it challenges the behaviour norms of many people. The book also challenges us to evaluate every expense in terms of the number of working hours it took to pay it.

In the recent couple of years, many millennials – including myself late “millennial” – have embraced pursuing the FIRE movement. In fact, I have always been a proponent of FIRE myself since I started working. The goal of the movement was to devise a plan to start work earlier, earn as much as you can and save a great deal from as young as possible. You add this to a good investment portfolio build over time and you are probably close to what you need.

Then comes the RE – you have the option to retiring early in your life.

FIRE devotees have been assuming the 4% withdrawal rule as a holy source grail that will supercharge and last for the rest of your retirement life. The 4% rule is the percentage that you can withdraw from your portfolio while keeping the rest of the balance intact and invested in the market with proper asset allocation.

In this article, we’ll do a couple of scenarios on the sequence of returns and withdrawals and see where it will take us at the end of our lives.

For the purpose of these calculations, I am going to add in a few assumptions first for the sake of it:

- Starting balance: $1m

- Current Age: 38

- Ending Age: 88 (50 years from today)

- Inflation rate: 2% p.a

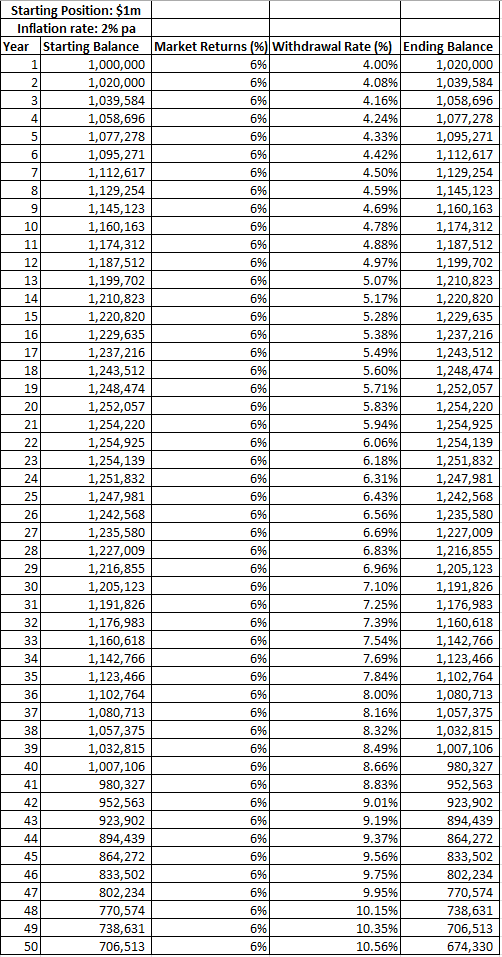

Scenario 1:

6% Flat Returns, 4% Withdrawal Rates adjusted for inflation

Scenario 1 assumes a 6% flat market returns throughout the period, with a withdrawal rate at 4% that are adjusted for 2% inflation every year.

Based on this scenario, you can see that the portfolio continues to increase every year until it reaches year 22 – that’s when it starts exhibiting declining balance because the withdrawal rate adjusted for inflation has crossed over the market returns of 6%.

You still end up at a decent $674k at the end of your life with pretty decent margin of safety, so this scenario qualifies for a tick in a box.

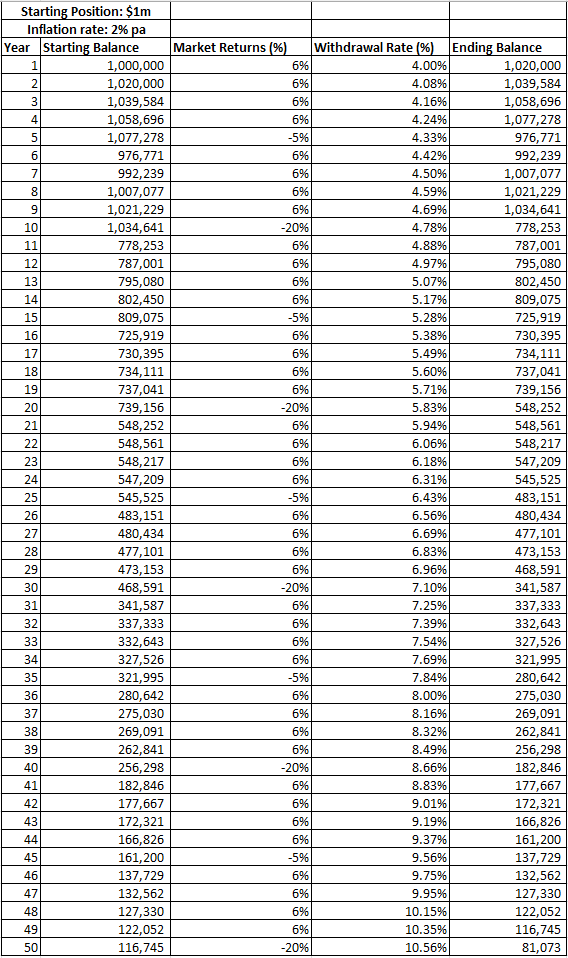

Scenario 2:

6% Flat Returns, 4% Withdrawal rate adjusted for inflation

+

5% correction every 5 years

+

20% drawdown (bear market) every 10 years

Scenario 2 assumes a slightly more realistic scenario, where it returns a 6% flat market returns throughout the period, with a variation of 5% correction every 5 years followed by 20% drawdown every 10 years for a bear market. The withdrawal rate will still follow a 4% per annum after which it is adjusted for a 2% inflation.

Based on this scenario, you barely make it “alive” with very little margin of safety left, especially if there are prolonged bear market cycle. Having said that, bull market often precedes a bear market, so you should get a theoretically higher returns as well to make up for it.

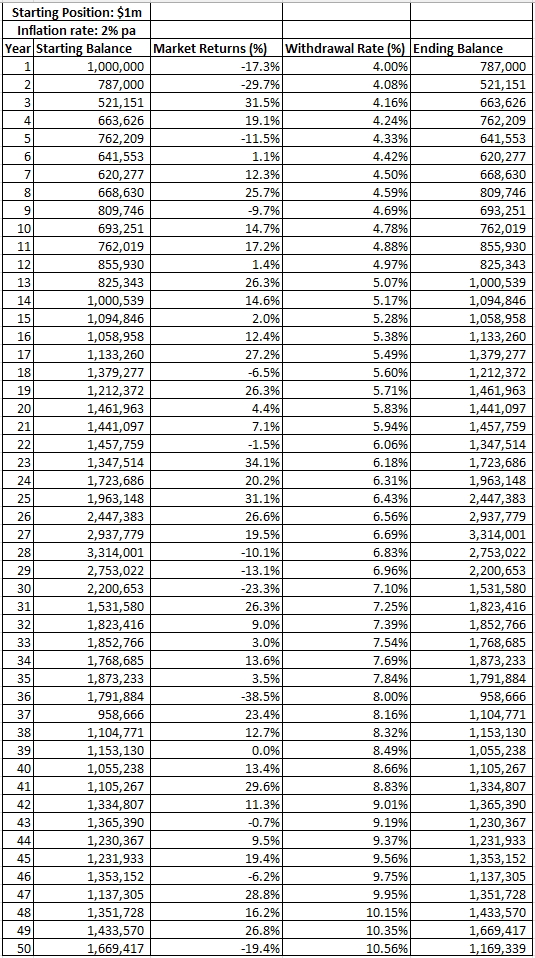

Scenario 3:

Real S&P Market Returns from 1972-2022, 4% Withdrawal rate adjusted for inflation

Scenario 3 depicts a very choppy real-life scenario where you might get double digit positive returns in one year and then a double-digit negative return the following year.

At the end of the 50 years, you actually end up pretty decent with over a million dollars left in your balance, although I’d argue it might not be worth as much in today’s present value.

Variations in Early Retirement Risks

Running out of money is not the only risks present in early retirement. There are tons of other risks to consider too such as health and mental, as well as families and friends.

While theoretically it is possible to have never “run out of money” using the simulation above, we’ll never know what the future 50 years might hold, so it is also important that you have other options such as annuities in place that will buffer should things go wrongly.

Start young, build more buffers, and continue to generate your own cashflow to tide through your retirement life.

If you have not followed my social channels, you may want to do so as I frequently post ideas and thoughts in those channels so if you are interested, you may follow me at my Facebook, Instagram or Twitter profile here.

Interesting numerical scenarios. It will be safer to use 3% inflation and 3% withdrawal rate. 4% withdrawal rate is probably risky.

Ya 4% rule was researched by William Bengen for 60-65 yr old retirees, not for 30-40 yr old FIRE’rs haha.

SOR risk is applicable to both 65 yo & 30 yo, just that the 65 yo has much bigger margin of safety. 60-65 yo can go with 3%-3.5% SWR with very high chance of not only outliving their portfolio, but also growing their portfolio to a few times the original size to pass down to beneficiaries.

For 30 yo FIREr to have similar chance may need 0.5%-1% SWR.