There was a time last year when one bad news after another just kept getting into Chinese stocks – in particular Alibaba and the media could not stop heaping onto it.

This year, it was the opposite, although I can’t help but feel the media was sensationalising the news a bit too much attention.

Ryan Cohen – the famous billionaire who built his fortune by co-founding online pet retailer Chewy Inc. and more recently cemented its position towards revamping Gamestop, has recently built-up similar stakes in Alibaba Group – with the intention to push for increase in share buybacks.

He believes that Alibaba could reach double-digit sales growth and nearly 20% of free cash flow growth over the next 5 years, which will benefit the company give today’s valuation puts them at only $300b market worth.

This is not the first time Alibaba has increased its share buyback. In fact, towards late last year, the company has decided to increase its buyback program to $40b, increasing it from the earlier $25b mandate. Cohen, however, believes they could go well into the $60b.

Much of it depends on whether the company believes it can use its free cash flow for higher internal growth or share buyback makes better sense because of its depressed valuation.

While retail demand and sentiments are likely to bounce back in China this year, we should not forget that there are strong competitions elsewhere from the likes of JD and PDD in the local scene, as well as Shopee and other e-commerce in the international scene. The company is also competing fiercely on the cloud segment with other players and financial gateway.

Apple Inc. – Case Study of Share Buyback

It should be noted that Cohen has built a massive stake in Apple himself, gaining a handsome 3-digit percentage profit returns over the years.

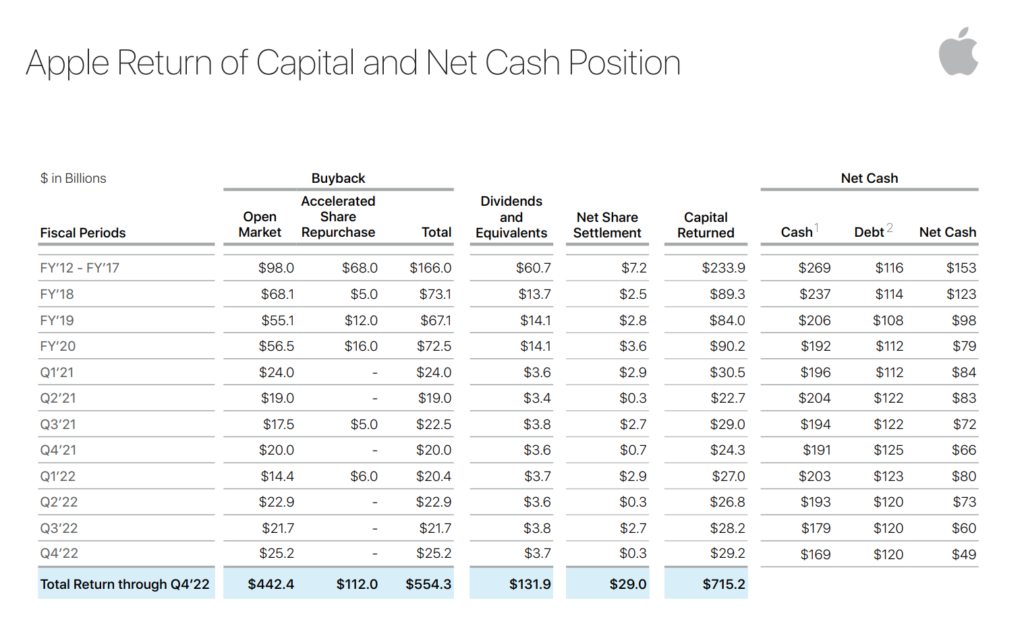

Apple was a successful case story, as its incredible moat position led to the company generating a handsome free cash flow over the years which then led to an incredible amount of net cash that they kept in their books.

Their goals were to keep net cash neutral – so they began doing massive share buyback which they believe were more rewarding to long-term shareholders than to give out chunks of huge dividends.

Apple FCF margins stands at a whisk away from their operating margins of ~ 30%, so they can keep doing this over and over again, and in the years leading to “undervalued” days, share buyback made the most sense to them, especially from 2012 to 2020, before the big jump thereafter that leads to today.

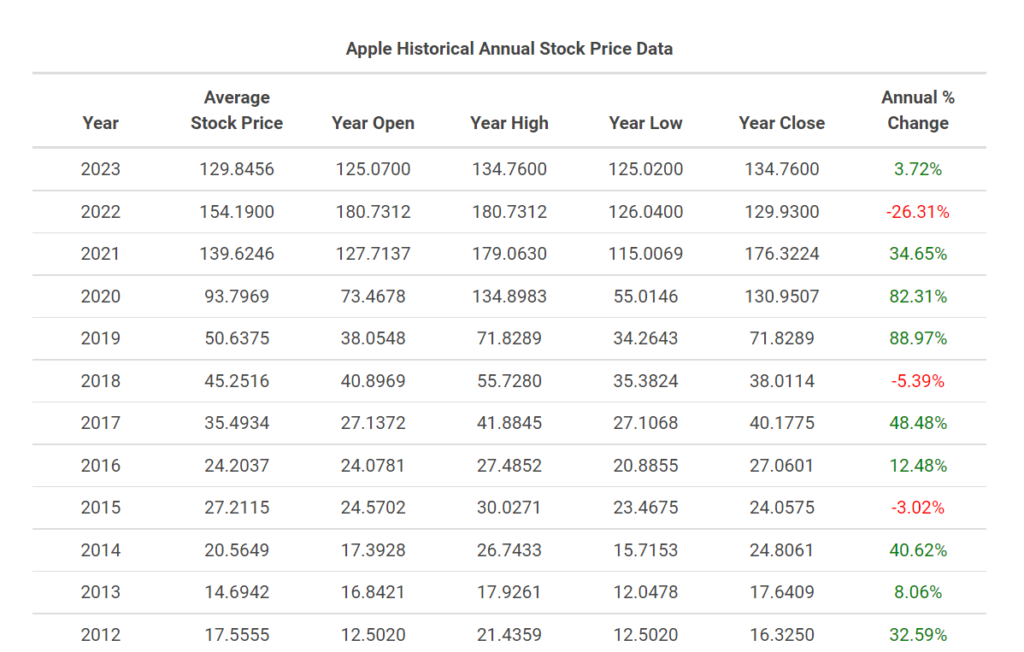

The resulting effect from this move was a rewarding return for shareholders as the stock has gone up approximately 210% over the last 5 years and 320% in the last 10 years.

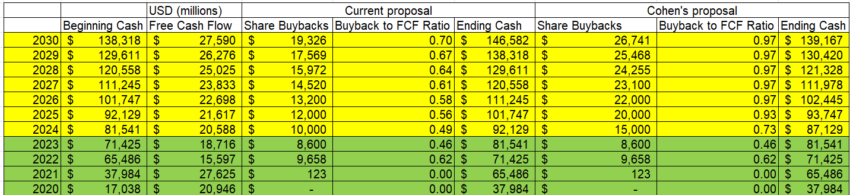

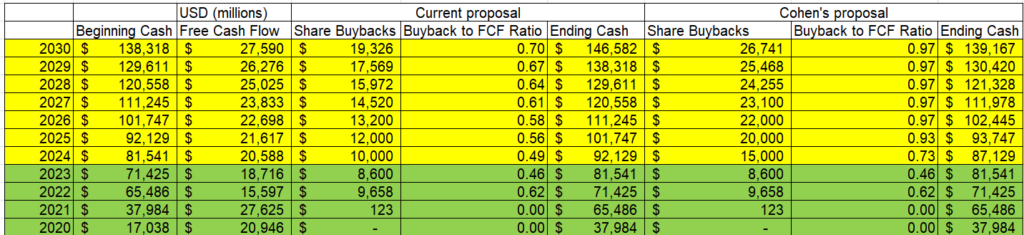

Alibaba Share Buyback Projection 2022 – 2030

I’ve drawn up a projection over the next few years leading to 2030 based on today’s current proposal repurchase mandate versus Cohen’s proposal to increase it to $60b until 2025.

I’ve kept the free cash flow growth constant at 5% growth from 2024 onwards all the way to 2030.

You can see that similar to what Apple was doing earlier in the years, Cohen is likely to propose a buyback that is nett to the ratio of the free cash flow. In other words, he believes that the company is better off buying back its own shares rather than using the money to fund its own internal growth. The goal is then to keep a net cash neutral after deducting all the short-term liabilities.

We’ll never know if this might work over the longer term for Baba as Apple was a different company and clearly in a dominate fundamental position when they did the repurchase cycle loop. Apple also benefited from the valuation on multiple earnings expansion when the stock price started to increase massively from 2018 onwards.

Whether this can apply to companies like Baba, it remains to be seen.

If you have not followed my social channels, you may want to do so as I frequently post ideas and thoughts in those channels so if you are interested, you may follow me at my Facebook, Instagram or Twitter profile here.