After the last hint on my July portfolio updates, we finally have some updates where we are moving next which we are ready to share.

Just to give a little context before I start, we bought this property which we currently stay in just right before the onset of Covid ~ 3 years ago when we decided to move out to a smaller home due to some financial situation after my Dad was hit by a stroke and we had to cough out a huge sum in the range of $200k-$300k for his medical bills.

Back then, I was enjoying my little moments of sabbatical onsets after I left my previous job so I was unemployed and there was no incoming source of income when all of this took place. After I found a job, we quickly applied and purchased our second “smaller” home.

Because our financial situation was not stable yet at that time, we decided to crash in at my in law place for about a year while we used this time to rent out both properties for rental income. For a few months during Covid, I also applied for the waiver of principal payment (interest still continue to accrue) from the banks and this further helped me built up my savings.

At about sometime in Dec 2020 when the Delta variant was about to stabilize (little did we know soon that there was a new variant called Omicron that soon arose), we decided to move in to our new place. You can find my compilation details of that move here in this article.

Reasons We Decide To Move

We have only stayed here for a considerably short time but we quickly fall in love with the place – myself particularly since I enjoy outdoor and it is close to the nature.

My wife loves the set-up of the study room we have, and given that both of us are on “Work from Home” order for most of the time, a comfortable set-up of a strong WIFI, a nice table and a steady working chair is all that we need to get the work groove going.

We do not drive so it is also important to have the good connectivity access to buses, MRT station and a mall – and we are privileged to have all three.

We were not planning to move out when we were having our holidays back in June and this decision was only taken and made after we came back in late June. It was a little impromptu and we admitted that we were somewhat taken aback ourselves by how fast things have moved.

In any case, here are our main reasons why we decided to move back to our old place:

1.) Proximity to an Affiliate Catholic Primary School

There is an affiliate Catholic primary school that is within 1km that my wife had always wanted to apply for both of our kids. When we moved out of our home 3 years ago, that dream was dashed and while we eventually had secured a similarly good school, that was still not our first choice.

With this move, there is a good likelihood that we’ll be able to apply for a transfer for the elder one and apply the 1km proximity rules for the younger one next year.

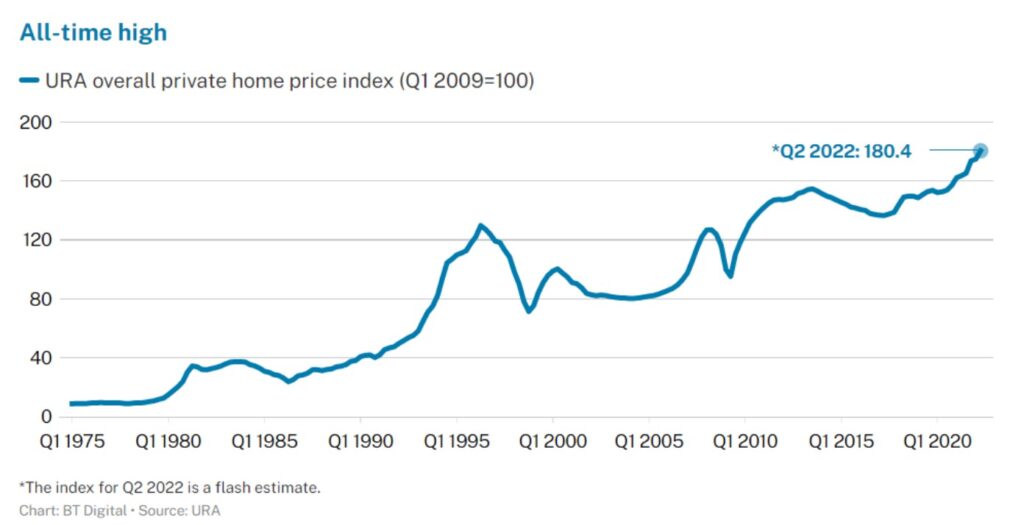

2.) Home Price Index At The Peak

The second reason has something to do with home pricing at the recent peak and we want to take advantage of that opportunity to divest one of the two private properties.

Overall home price transactions and volume have spiked up considerably especially over the last two years as inflation bites which sends asset prices roaring high. Despite the various cooling measures being introduced, the demand for housing continues to increase steadily due to both local and foreign demand.

In my part two of this series, I’ll share how I come to know about these information when I get first hand information from buyer and tenant themselves.

3.) Interest Rates Are Rising

I’ve been writing articles over the last couple of months asking homeowners to quickly lock and secure their fixed rate before it goes ballistic.

As most of readers on this blog would know, the US is doing quantitative tightening due to hot inflation situation and this has forced the Fed to increase rates in order to curb the situation and bring it under control.

Higher interest rates mean that more allocation of your monthly mortgage payment goes to the interest rates rather than your principal so your equity will go up lesser than it should in the past. Generally, it does not benefit debt payers as you are paying more for your interests.

While we are apparent and aware of the interest rate rising – we have previously locked in a good low rates for about 2 years but we’ll never know how things might turn out after that. One of the ways we can eliminate this risk is to reduce the debt that we have.

4.) Potential Boost to Warchest

You never know what shock you are going to get from the economy and the market in the short term – which means it is probably safer to keep part of them as cash for the time being. Longer term, holding cash was never the answer as it quickly usually erodes out in value.

As for now, we are opening up for both possibility for both rent and sale and see how the demand goes from there. If a sale happens, then this point would be more relevant.

5.) Bigger Space

The other place we are moving into is an older development and because of that it has bigger space and more rooms.

This will work in favor once our two kids grow up eventually and each of them require a room each, so we are thinking obviously much longer term.

So that is it for now – in my part two of this series, I’ll give an update of how and if we manage to lease out or sell the property based on the demand and viewing so far, and how much returns are made from this investment-home double down.

If you are interested in my property series, I have a page dedicated to this. Do keep a lookout for more home and property series in the future.

If you have not followed my social channels, you may want to do so as I frequently post ideas and thoughts in those channels so if you are interested, you may follow me at my Facebook, Instagram or Twitter profile here.

Dear Brian

Best wishes for your move and good luck for the proposed sale

Regards

Garudadri

Hi Garudadri

Thank you, and finger cross hopefully some good news soon.