First of all, Happy New Year to everyone!

This would mark the first post of the New Year and I wanted to start with something that is light and close to every Singaporean’s heart, and being in this fanatically finance driven friends around you, that would mean the start of the Year will always be marked with a new CPF balance.

I was told that the CPF website was under maintenance last night when the clock strikes midnight so for those anxiously waiting many have to wait until early this morning before they can start logging in.

I was alerted by the flurry of news and also logged in this morning, curious to see how I did for the year 2021 especially since there were only drawdown via OA for housing with almost no voluntary top up due to the shortage of cashflow.

To my surprise, the compounding does takes into effect rather quickly every each year that goes by.

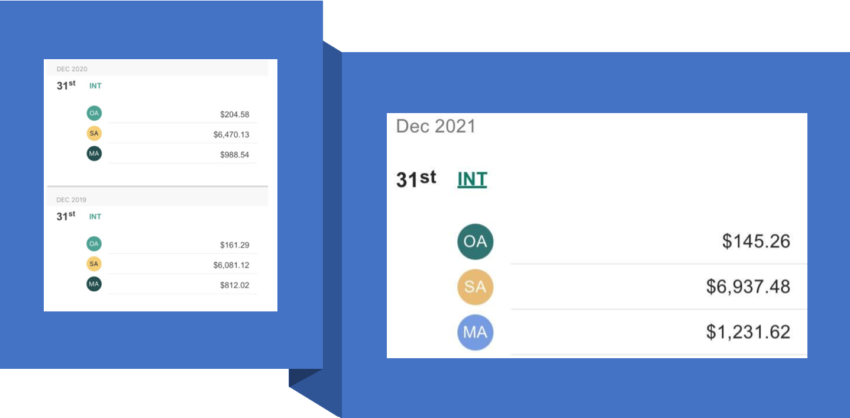

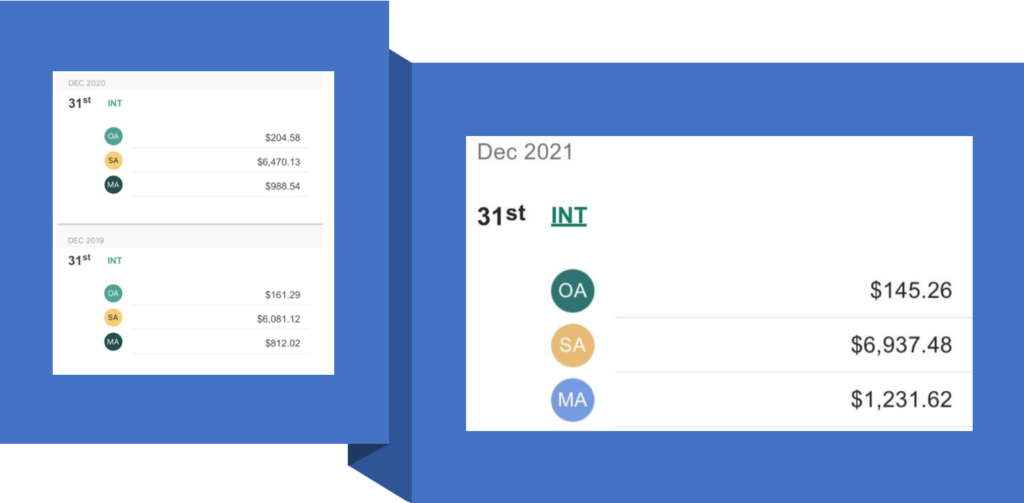

Last year total interests was $7.6k and this year it is $8.3k – an increase of about $700 in the space of a year.

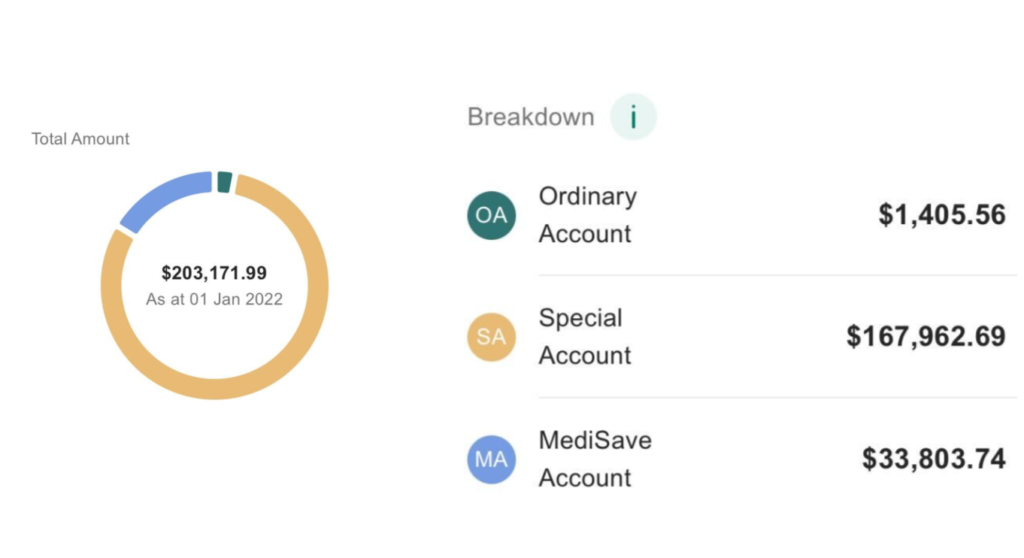

However, this did not manage to bump up the balance significantly as I have continuously exhausted my OA account for housing mortgage each month so the overall CPF balance only increases marginally from the previous year of $200k to this year of $203k (everything combined).

I do not foresee any of my strategy would change from here in the near term so I’ll leave this passively managed bond-alike structure to remain in my back pocket for a while.

Meanwhile, FRS for 2022 has increased to $192,000 (increased from the previous year of $186,000) so I am likely to lag behind the FRS for the next foreseeable years until something miracle happens.

Dun lose hope, funnel whatever u can spare this yr into your sa!:)

Thank you, I will try my best to channelling any bits at a time so it doesn’t feel much.