Tencent Holdings Ltd is one conglomerate company in China which has triumphed and dominated so many winners in the past few years that it has become increasingly difficult for investors to buy in and own them simply because they keep on getting better and stronger each year.

In fact, if we look across the past 10 years of making for Tencent, the best time to buy and own the shares is the day the company is making its 52-week high because you know they are just going to beat that record on its own down the road.

The only 2 meaningful times which investors can get in at a reasonable valuation after the huge run-up was back in 2018 due to a regulatory crackdown which they’ve dropped 49% from peak high and then today in 2021 which they’ve dropped about 42% to date.

In this article, we’ll be mainly discussion on the valuation model of the company to see how much they’ve grown over the past few years.

Weixin + WeChat + QQ IM

– Almost The Entire China Population

For those who are not familiar with the product offering and services which Tencent is currently offering and how the company is monetizing them, you may want to read here.

In essence, most of the stuff they are offering to their citizens are free in nature, so there is no real agenda push where users might drop off once or twice after using them.

The big 3 – which is Weixin + WeChat + QQ – are essentially your everyday needs from chatting, entertainment, payment and many more. I just don’t think anyone that lives in China can survive without having these apps installed on your phone.

If you look across the monthly active users (MAU) which is a key metrics to how much a company has dominated the market share, you may be appalled to see just how much they’ve grown over the past couple of years.

As of the latest Q1 FY2021 results, MAU for Weixin + WeChat is at 1.24 billion and MAU for QQ is at 606m.

To put things into perspective, China has a population of over 1.4 billion so that gives you an indication of just how much market they’ve captured in China.

Regulatory Crackdown 2021 Impact on Valuation

Tencent Holdings earned their revenue from a few streams.

One of the biggest chunk of their revenue streams are coming from Games, which they’ve earned over RMB 43.6 billion in the Q1 of this year alone (total revenue is at RMB 135 billion). If you are unfamiliar with some of their monetization model for Games and pipeline, you may want to search for my other articles on Huya or click the link which I’ve provided at the beginning of the earlier paragraph on the business model.

The next big chunk of their revenue comes from social networks and chatting which includes the advertising channel that they earned. In Q1 alone, they’ve earned RMB 50.6 billion in total for the VAS and Advertising segment for their social networks and media.

Other than that, they also other Fintech and Business Services which made up quite a huge chunk of their portfolio as well.

The regulatory crackdown that is impacting businesses across has some but little to impact the fundamentals of the company.

For instance, minors aged 18 and below accounted for just 6% of Tencent’s overall online game receipts. Among which, a subset of those under the age of 16 accounted for just 3.2% of the online game receipts.

If we look across the entire regulatory impact of not allowing minors under the age of 12 to play, or limit the number of hours minors under the age of 18 can play, the impact to the Gaming segment would be limited to within 2-3% at best. To the overall entire revenue segment, this would then make up 3% x 1/3 = less than 1% impact to the entire business stream.

The other regulatory crackdown on the education sectors might have a bit more impact to the advertising as well as its Fintech SaaS business.

In the 2020 annual report, Tencent specifically singled out education, internet services and ecommerce platforms as one of the main revenue generators from online advertising. Given the recent regulatory crackdown on education companies, we can expect this portion of the segment to be significantly hit. Assuming the education business makes up a total of 10% weightage, this would mean a hit of between RMB8-10 billion in advertising revenue in a year.

Impactful but is unlikely to bring down the company.

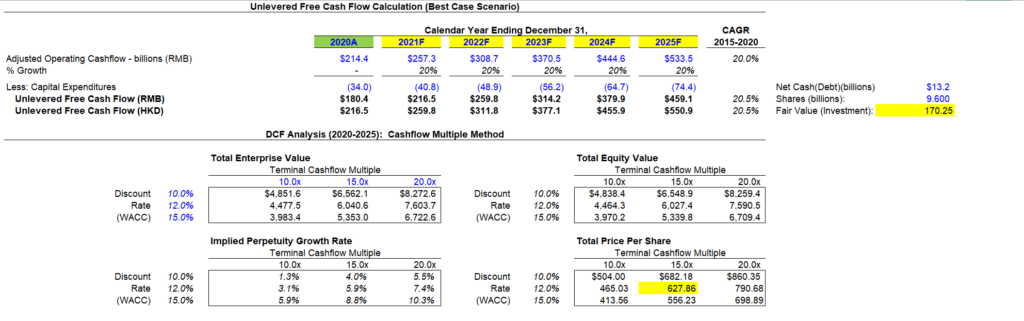

DCF Valuation Model + Fair Value Investment

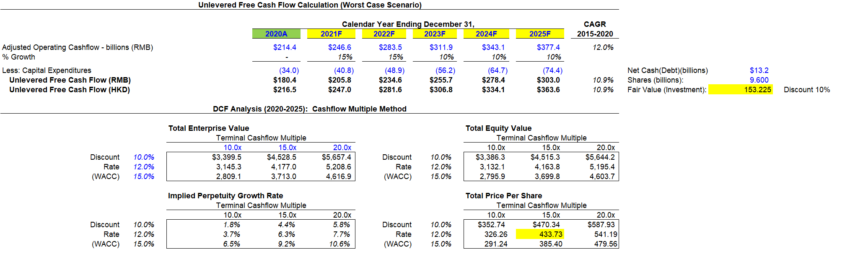

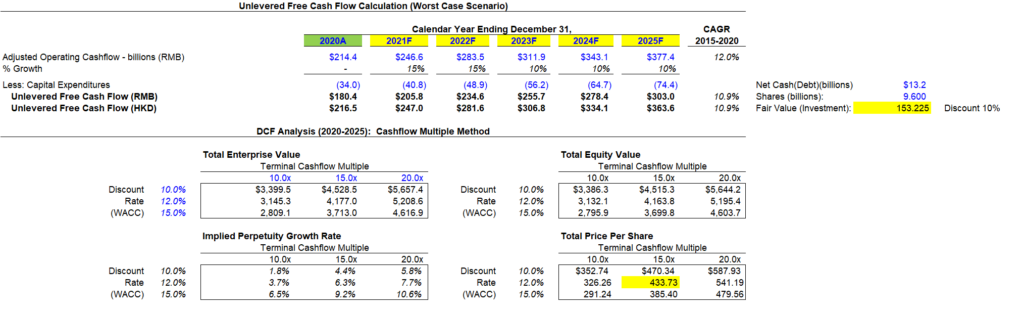

The base case scenario embeds a model of 20% growth for the next 2 years, then 15% for the next 3 years.

Capex spent is mainly on operating expenses for their media content as well as their non-operating expenses on lease liabilities.

For years, Tencent has a habit of spending and reinvesting their entire free cash flow into new businesses and do not maintain a huge chunk of cash on their balance sheet (Net Cash equivalent is only at RMD11 billion) so we will assume the same in the model.

These businesses are recorded as part of their equity share of profits and not into the organic model of their operating cashflow so we’ll have to add that in at the end of the day.

As of 31 March 2021, the Fair Value of the shareholdings in listed investee companies, excluding subsidiaries, stand at RMB 1.36 trillion, which if we compare into HKD/share, it is approximately worth HKD170 (RMB 1.36 trillion x 1.2 HKD / 9.6 billion outstanding shares).

If you’re interested to look at each of the investment, you may look at this sheet which another blogger has compiled. Do note though that it may not be updated on a daily basis, so I would still look at the fair value from the official financial reports every quarter for better clarity.

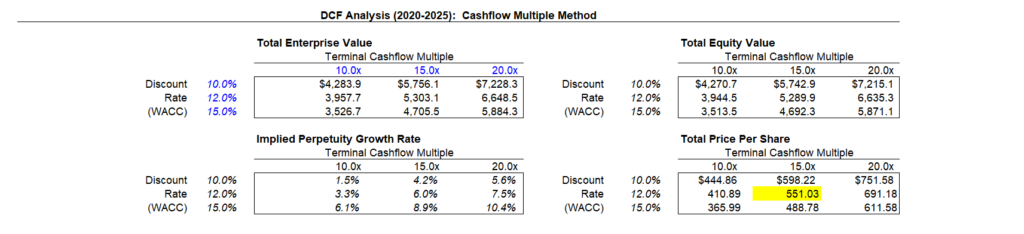

To continue with our DCF model, we have input a terminal cashflow multiple sensitivity of 10x, 15x and 20x and a discount rate of between 10 to 15%, with 12% in the middle range. This discount rate is the expected return that we as investors are trying to get or achieve over the longer term.

The base assumption leads us to a share price that’s worth HKD 551.

Together with the earlier fair value investment that we’ve computed which is worth HKD 170, the intrinsic value for the company should be worth HKD 551 + HKD 170 = HKD 721.

Do note that this is the base case scenario.

If you’re trying to project a worsen or better scenario, the number would then also shift accordingly.

So to do a quick one, if we are trying to project a worsen scenario, we would use the assumption that the company will only grow at 15% over the next 2 years and then 10% over the next 3 years.

I have also discounted the fair value investment by 10%.

The intrinsic value that I get out from this assumption is HKD 433 + HKD 153 = HKD 586.

If we’re trying to pull out a stunt and do a best case scenario where the company is able to maintain a 20% growth throughout the next 5 years (not impossible but improbable), we’ll get an intrinsic value of HKD 627 + HKD 170 = HKD 797.

But I’d likely wouldn’t count on that as an investor trying to be conservative.

Conclusion

The DCF model is trying to give a sense of range of just how much can the value of the company be worth even with all the regulatory crackdown impact in place.

As an investor, I try to see what’s my conservative scenario, and then look at what the market is valuing the company today and see if there’s a good opportunity to load into these businesses.

From my personal portfolio point of view, I have since more than 9x the value of my investment in Tencent since last month so it’s becoming a large part of my portfolio. I do really think that while the crackdown provides uncertainty to the businesses in the near term, they are unlikely to severely impact the overall business in the longer run and current valuation is simply to hard to resist at this point.

Hi Brian, am curious, for your Tencent foray, why in HK mkt instead of US?

Hi YJ

Sorry for missing your reply.

The US market for Tencent is an OTC which has lesser liquidity and have lower flexibility in terms of not being able to trade pre and post market as well as no options market.

uncle168,

this b1617 kill rate is very high. everyday 1 elderly uplorry still the gov open up.

covid spread via social contact, isolation is the only way to minimise the death rate.

once we open up on 10 aug, 2 weeks later the covid cases will start to rise exponentially again from 23 aug.

the ktv case started 2 weeks after the last opening up of 2 person dine-in.

every day 2 person would die from covid and 50 need o2, most of them would be fully vaccinated as they are now allowed to dine in groups of 5 exposing them to the deadly b1617.

the gov is using the opportunity to test whether fully vaccinated will die or not if they socialise.

the vaccinated idiots will go and dine in in groups of 5.

those who believe in the vaccine will soon get to see heaven and join lky with their stupidity that the virus is afraid of the vaccine.

by mid sep the gov would lock down again, the vaccination narrative would change from:

1. vaccinated will not get covid.

2. vaccinated will get covid but will not get seriously ill.

3. vaccinated will get covid but FULLY vaccinated will not get seriously ill.

4. FULLY vaccinated will get covid and can get seriously ill but not die.

5. FULLY vaccinated will get covid, can get seriously ill and die but a THIRD dose will help.

the final narrative would be what i’ve said all along, vaccination is useless like mask.

only complete closure of borders, total isolation via wfh, dabao and relying on domestic consumption and financial sector can help us keep death rate very low and the economy flat.

the gov ding dong method will just make the people more and more angry.

the gov has to tell the people the truth that covid will wipe up the human race eventually and by isolating ourselves we can spread out the death rate until we find a real cure for the disease.

covid is like hiv and sars combined, it is lethal yet it can spread quickly.

it doesn’t die out like normal virus because it is man made by the ccp gov to wipe out the amdk.

now china kenna karma as b1617 go 1 big round and go back to china.

the gov refuse to acknowledge the reality of the pandemic and keep trying to open up, this would result in high death rate to its citizens by the end of august.

look at the olympics in japan, the bubble kept cases low while in japan cases surged.

what does it means?

it means isolation is the only way to spread out the death rate until a cure is found which is unlikely as aids have no cure.

dinosaurs became extinct after the ice age, the human race wil become extinct due to covid.

god speed.

keekeekee.

uncle168,

a country divided due to the class war created by 56 years of state capitalism best describe this year national day.

ever since lky and gct got kicked out of the cabinet, massive influx of foreign labour created 2 decades of crude economic growth not from gains in productivity but from doubling the population thru immigration.

this created 2 problems, rising death rate due to ageing and falling birth rate due to high cost of living. in 50 years time stinkies would become extinct.

during covid the gov used s$100b to bailout the banks and landlords. jobless stinkies became food delivery rider or safe distance ambassader.

the distrust of the gov became so bad the gov have to ask keppel to bail out the local newspaper which nobody reads any more.

leadership transition was missing due the lack of conviction that pap was leading the country towards the correct path and the current leader place himself above the nation. lky planned his succession the day he was appointed pm. hsk likely stepped aside due to his dismay performance in ge2020 in ec grc. now we run the risk of going without a pm should lhl up lorry.

the old model of a rent seeking economy fuelled by massive immigration no longer works. the rat race cause our youth to commit sucide and few chase the rainbow or dreams as there were no assurance of a pot of gold at the end hence our zero medal tally at the olympics

the ding dong method used by the gov made life miserable for stinkies and frontliners. trying to open up when they know will end up closing soon after is a waste of resources and time. crisis presents opportunities in banking, ecommerce, healthcare, logistics and manufacturing where labour can be reallocated from sectors like tourism and aviation.

fear of covid death made stinkies part of a global vaccine experiment when the long term effects are unknown. 98% whom get covid eventually recovers whether vaccinated or not. vaccination injuries and death are dismissed due to pre-existing disease while non-vaccinated covid death were dismissed due to not being vaccinated when the reason of death is due to pre-existing illness. oyk has blood on his hands as he get his bonus for hitting his vaccination kpi as the hell gate open in the 7th month the vaccinated death look for him for answers. my father is vaccinated as he fears dying of covid. my mother isn’t as she fear dying from the vaccine. i’m not vaccinated as i believe the vaccine is useless and has adverse long term effects on fertility, heart, kidney and brain function.

racism is a spinoff from the actual problem, the class war. chinese have become rich while most malay remained poor, this spark off race issue like hdb flats and rights to buy waffles.

capitalism has failed to trickled down. immigration has divided us. we do not have a new leader. trust in the gov has eroded. stinkies will soon become extinct.

we did it before because of lky’s conviction.

we will not be able to do it again as we are divided by the class war.

happy national day!

keekeekee

uncle168,

by 24 aug the icu will be filled with fully vaccinated elderly whom has dined in groups of 5.

the gov would ban elderly from dining out until they get third shot.

many vaccinated youth also need 02 as they go gym and eat in group of 5 rapidly infecting schools & workplace.

the 5g leaders stupidity will be known globally thinking b1617 is scared of the vaccinated.

the vaccinated idiots is helping b1617 spread and mutate rapidly via social contact.

we could soon see a new sg varient as the gov also ask hiv patient to get vaccinated, the perfect host of a super mutant.

keekeekee

uncle168,

now 33% in icu is fully vaccinated.

by the end of august 66% in icu will be fully vaccinated.

by beg sep fully vaccinated children will end up in icu and 88% in icu will be fully vaccinated.

by mid sep the gov will lockdown again as the hospital run out of icu beds.

fully vaccinated dine out in groups of 5 would be the main catalyst in a spike in icu cases.

it is because people who take the vaccine thinks they are protected when in reality they have become victim of false hope and would pay the price of death for their stupidity.

the vaccine has zero protection against covid as the virus has mutated and evaded the immune response of the vaccine.

it would be divine retribution iif our leaders end up in icu by discriminating the smarter non vaccinated..

the gov roadmap leads us in circles.

we should have a long term isolation strategy like china instead of wasting time dreaming of opening up.

we will lock down in mid sep again as children begin to die from covid because the gov kept school open thinking the vaccine would protect them.

keekeekee