I’ve been receiving tons of questions on my emails since the last couple of posts from readers asking me if it is a good time to enter the Chinese tech market and what’s my current my average costs on some of the companies that I am still holding so far.

Now, I’ve been writing regularly about my personal take on the overall Chinese tech market so I think you’d be bored to have me repeat it again here.

I also do not have the obligation to share each of the position I bought and sold at any point in time but I have regularly done it anyway through my monthly portfolio updates.

In the spirit of sharing and transparency, I’ll also share my average costs on these companies since I have many readers who were asking them.

Personally, I’m using the average costs on my position to gauge my entry level capability to ensure I am not paying too much for a position which I think doesn’t make sense. It also helps me to gauge at which point I should be averaging down and how much buffer I have before I’m wiped out by the margin I took in a worst case scenario (Yes, there’s a lot of calculations and considerations taken behind the scene which I’ve done on a regular basis such as how much drawdown and income I’m receiving in the next few months, etc).

At no point in time this should be taken as an investment advice for a good entry position as our circumstances may be different from one another so some disclaimer there.

Here we start.

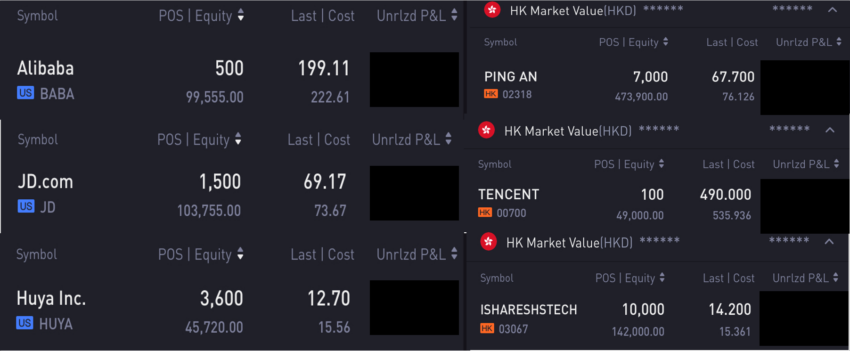

Alibaba (NYSE: Baba)

First up is Alibaba.

My current average position is at US$222.6, and this was mostly initiated when I wrote the article back on the 2nd July when I mentioned that Baba had a breakout which I thought was the key point for a reversal of a trend.

Unfortunately, the China tech clampdown continues to escalate and this brings Baba back to below the important trendline (at about $216.5 now) which they have also recently tested twice the resistance but failed to go up higher.

With the entire sector now having a massive fear factor, particularly the recent Edu tech sector, Baba was one companies that were being dragged down by the news.

The current paper losses to date amounted to US$11,750 or 10.5% – which is about SGD 15,750 roughly if we convert it back to Singapore dollars.

JD.com (Nasdaq: JD)

Next up is JD.com

They are in a similar space as Baba so they are pretty much “together” when it comes to either rallying or falling.

My current average position is at US$73.6, which I believe remains at very decent level going into this long drawn battle. In fact, I had added a position into JD roughly about the same time as I have added Baba so the same reason applies to this one.

If you are interested to read my DCF valuation analysis on JD.com, you can refer to the article here.

The current paper losses to date amounted to US$6,745 or 6.1% – which is about SGD 9,000 roughly if we convert it back to Singapore dollars.

Nothing to worry for now – I believe that the average costs level is a decent take.

Huya Inc. (NYSE: HUYA)

I’ve also written a couple piece of articles on Huya, and its close competitor Douyu.

This is a little tricky because they are a smaller cap and in a sector which the CCP might relook and see any further restrictions they want to undertake apart from disallowing the recent merger case. The last restrictions was undertaken back in 2018 when they had to ask companies to abide by the license requirement and disallow teenagers from gaming after 10 clock on weekdays.

My current average position is at US$15.56, and this is mostly the underlying strong support which have been previously tested a couple of times but broken this time round. Still, if you read my previous article on Huya, you’d know that the market is cheaply valuing this company on an enterprise basis. Still, the sustainability of the company continuing to remain listed as ADR in the US indices remain a question.

The current paper losses to date amounted to US$10,280 or 18.4% – which is about SGD 13,775 roughly if we convert it back to Singapore dollars.

Ping An (HK: 2318)

I’ve been wanting to write an in-depth article on Ping An for the longest time but has never quite yet finished my research on some of the points I’m still trying to look for.

Ping An is a little tricky because as an investor, if you are just scratching the few financial reports, it looks like there’s nothing inherently wrong with their fundamental but they are actually undergoing a few transition within the company that are slowing down some of the segments in their business.

Coupled that with the recent flood case happening in China, where insurers are likely to make a pay out (not sure the quantum), it does look like bad news one after another that’s coming to haunt them.

My current average position is at HKD$76.1, which I believe remains somewhat decent from a historical valuation perspective but may took slightly longer to rebound if the transition piece turns out to be slower than expected. Still, the company gives out dividend of around ~4% at current level so that’ll be some consolation as we wait for the price to recover.

The current paper losses to date amounted to HKD$58,982 or 11.1% – which is about SGD 10,200 roughly if we convert it back to Singapore dollars.

Tencent (HKG: 0700)

This is a relatively small position for now.

I’ve previously added when they managed to hit the EMA50 support at $530 and hold that line for quite a bit but today’s price action proves to be too much for them as they went down by as much as 7% in today’s trading, ending at a low of HKD$490.

My current average position is at HKD$535, and I’d be looking to add more to my position as it trends lower or soon once the unrealized losses hits > 10%.

The current paper losses to date amounted to HKD$4,593 or 8.6% – which is just about SGD 800 roughly if we convert it back to Singapore dollars.

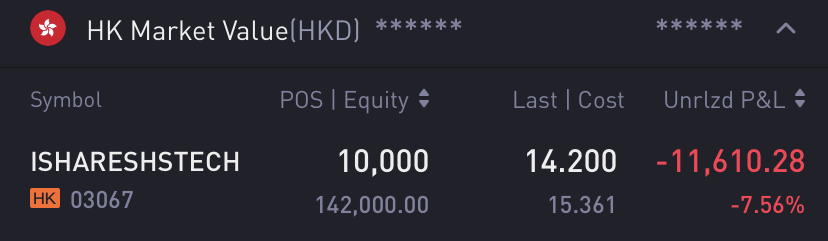

ISHARESHSTech (HKG: 3067)

This one is an index ETF which tracks the top 35 components of Chinese tech companies and powered by Blackrock.

I bought this as part of my diversification looking outside the individual tech companies I already have in my position but yet still wants direct exposure into the position.

My current average position is at HKD$15.3, and I’d be looking to add more to my position as we see lower price action and more fear coming into the market. At this average price, I really feel it’s hard to go very wrong and it’s just a matter of endurance and patience before we see this in the green.

The current paper losses to date amounted to HKD$11,610 or 7.5% – which is just about SGD 2,000 roughly if we convert it back to Singapore dollars.

Final Thoughts

To sum the total losses to date, I have accumulated around S$51,525 in unrealized losses so far for the abovementioned positions I held in Chinese tech stocks but like what most seasoned investors in the world will say, sometimes you have to go through this in a bear market in order to turbo engine your portfolio further.

In fact, during the depth of the Mar 2020 COVID crisis, or even prior to that, such as the 2011 Euro crisis, 2016 China and oil crisis, 2018 Trade War, I have accumulated more losses than today and still managed to get rewarded handsomely when things rebounded back thereafter.

It’s quite common to see people openly sharing their winning positions but not on their losing positions so I hope this article helps in circulating back some of your thoughts in the respective positions you have so you can do the proper calculations and considerations accordingly like I do.

Buy more? DCA?

Yes, of course! Chances don’t come everyday like this.

Thanks for being so transparent Brian! Now with the ccp coming out to reassure the market, not sure I can scoop another round not haha.

Thanks for sharing..

Thanks for sharing . Always impressed by your transparency and thought processes.

I am worried as well whether this would be a larger or more permanent change . Since CCP seems committed to making quite a few changes, and unlike the US , they have the power to break up companies and monopolies (which Alibaba in a sense is, since it created a monopoly using capital/anti-competitive practices).

“It’s quite common to see people openly sharing their winning positions but not on their losing positions so I hope this article helps in circulating back some of your thoughts in the respective positions you have so you can do the proper calculations and considerations accordingly like I do.” truer words have never been said.

Personal take on Ping Ann, i tend to stay away from investing into the Financial Service space in China (i’m invested indirectly through A50 ETF), as its a real value trap.

Food for thought from Bloomberg a year back, still holds true IMO –> https://www.bloomberg.com/news/articles/2020-09-08/chinese-bank-stocks-lose-187-billion-in-never-ending-value-trap

better cut loss on chinese stocks now… for me i lost alot already. don’t want to gamble anymore…

Hi Sim K

I’m sorry to hear that but as long as you find peace in your decision, it is worth it.

What do you think of Ping An now?

Hi JJ

Sorry for the delay!

I am still bullish on Ping An and managed to add a little when the stock capitulated recently down due to the Evergrande news. Still holding on to losses at the moment though.