Yixin Group Limited (HKG: 2858) shares have had an impressive past couple of months, gaining +16.2% YTD after a shaky period beforehand. This outperforms the HSI index which at the moment YTD has only gained +2.5%.

The stock is currently under consolidation mode for about a month now going directionless.

With the recent rebound in share price, there still wouldn’t be many who think that Yixin Group’s Price to Earnings ratio of 7.5x is worth a mention when the median average Price to Earnings for the sector industry is about 18.5x.

One possibility for the relatively moderate P/E is because investors might not be confident of the company’s earnings going forward. The stock market is usually forward looking so investors can only say with confidence once they see a clearer growth direction going forward.

Business Overview

Yixin Group Limited is a prominent player in China’s online automobile finance market. Founded in 2014 and headquartered in Shanghai, Yixin operates an extensive online platform that facilitates automobile transactions and financing. The company operates through two main segments: the Transaction Platform Business, which primarily supports auto loans through partnerships with financial institutions and offers additional services like SaaS and guarantees; and the Self-operated Financing Business, which provides direct auto finance solutions including leasing and sales-and-leaseback services.

Yixin’s platform, comparable to e-commerce giant Taobao, offers a comprehensive suite for buying, trading, and financing vehicles online. This model has driven significant growth, highlighted by their successful IPO in 2017, which raised HK$6.77 billion and became one of Hong Kong’s hottest IPOs.

The company has been backed by major investors including Tencent, JD.com, and Baidu, which collectively hold substantial shares. Yixin’s revenue streams are diversified across facilitating transactions, offering financial leasing, and expanding into related tech services.

Despite the broader economic challenges in China, Yixin has focused on staying within its core competency of auto finance, recently divesting from a joint venture that was expanding beyond auto-related services. This strategic focus has allowed Yixin to continue growing, particularly in the electric vehicle (EV) financing sector, which saw a significant year-on-year increase in loan facilitation.

Competitive Landscape of Auto-Financing

The auto-financing concept is not new and has in fact been around for decades.

Just like purchases of other big-ticket items such as housing, banks would traditionally be the biggest beneficiaries of such financing, given the nature of its business.

There are generally four types of auto-finance providers:

i.) Banks or Financial Institutions

ii.) Automaker backed auto finance companies

iii.) Auto dealer backed auto lease companies

iv.) Online auto transaction platforms

Let us take a look into each of these providers.

Banks, for obvious reasons, enjoy the advantage of the lowest cost of funding. While banks have their own networks to access customers, their focus is usually not towards sourcing and they would rely on third party platforms or providers to refer customers to them. Furthermore, banks typically take longer for approval as their processes are a lot more stringent due to requirement.

Compared to banks, automaker backed auto finance companies or auto dealer backed auto lease companies have usually higher cost of funding, but they are well distributed within their own network and can even cross-sell other financial services other than cars, for example personal loans or car insurance, etc.

The biggest advantage of an online auto transaction platform is the technology behind the big data capability that allows them to not only source for potential clients, but also conduct and analyse the applicants’ creditworthiness, process documentation, provide a more friendly efficient end-to-end process, and is usually more lenient towards individuals with lesser than desired credit score.

Where is the Opportunity?

For the fiscal year 2023, Yixin Group reported notable financial performance.

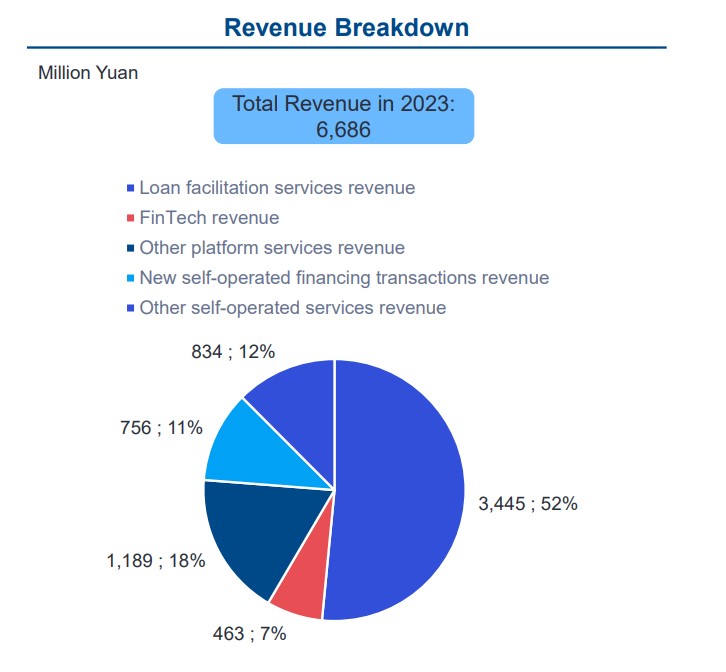

The company achieved a revenue of ¥6.7 billion, which is an impressive +29% YoY growth, with a gross profit of ¥3.7 billion.

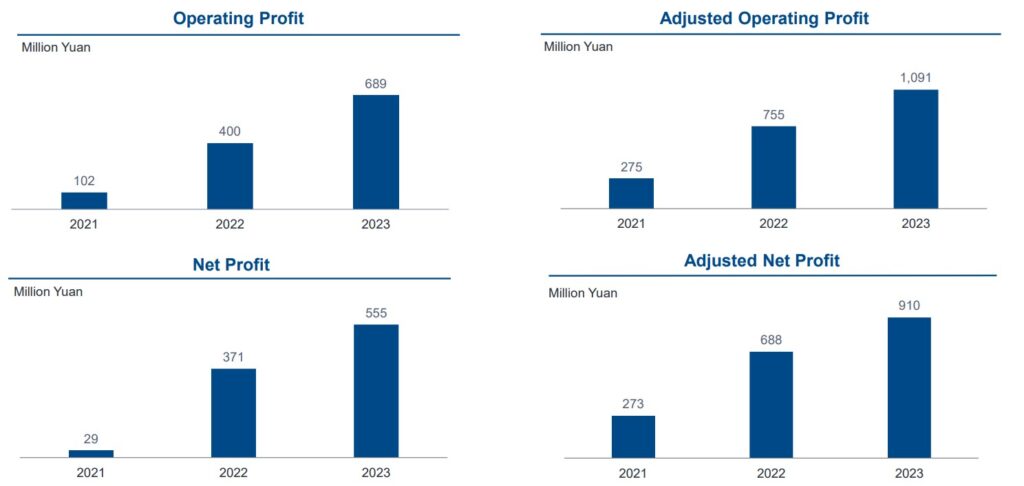

Net income for the year amounted to ¥555 million.

Additionally, the company’s earnings before interest and taxes (EBIT) were reported at ¥1.5 billion.

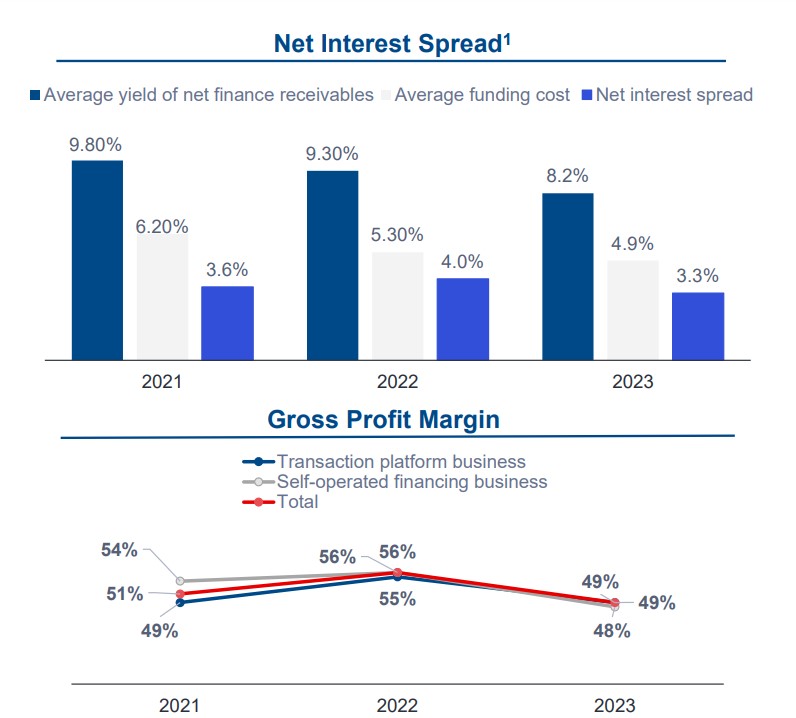

The company continued to earn a healthy gross profit margin despite the tightening in the net interest spread this year.

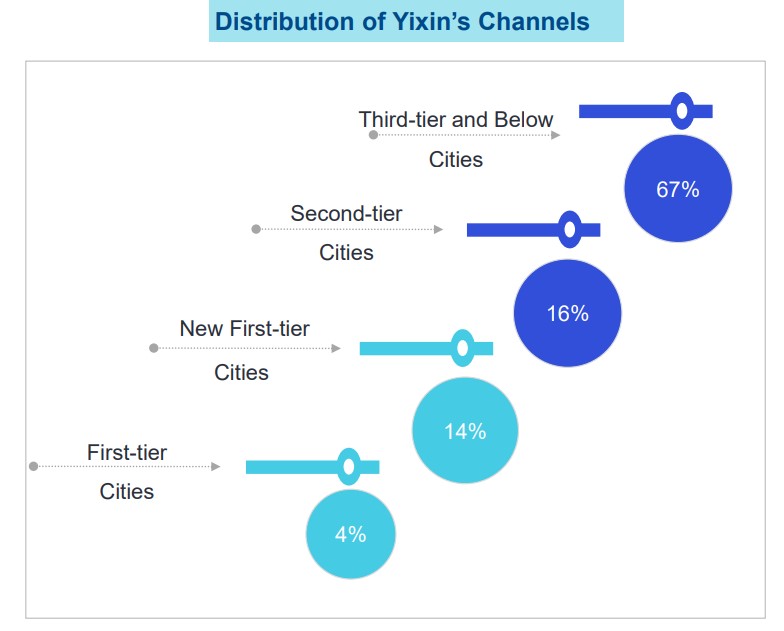

One of its strategies for this year is to tap into the lower-tier cities as the company believes it is still relatively untapped in the NEV segment. This gives them a projection target of 16% for the second-tier cities and 67% for the third-tier cities and below.

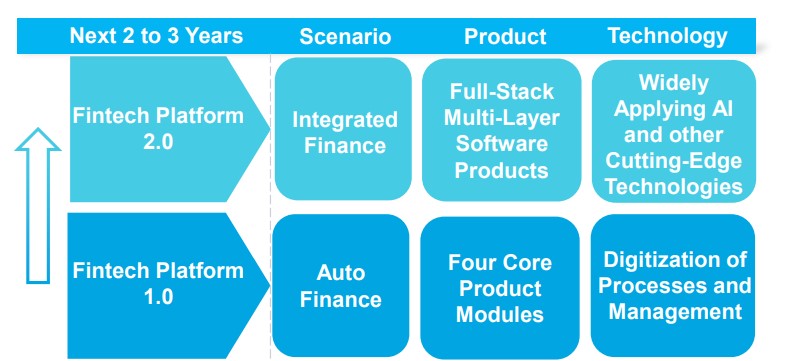

It is also looking to invest heavily into the fintech side of the business by investing in auto-financing platform that will allow them to tap into the mass market before hunting for the premium market share. The company pledges to spend as much as 50 billion Yuan to make this happen in the next 2 to 3 years.

Turning to the outlook, the next 2 to 3 years should continue to allow them to generate growth of ~20% per annum while the industry is forecasting an expansion of about 16% in the market.

We should see Yixin Price to Earnings reverting back closer to the industry average which even at 10x forward Price to Earnings would put their market cap at approximately double to where they are today.

Follow me, if you have not, on my social media channel here!