A lot has happened since my last coverage on Netflix which was many quarters ago.

Since Netflix’s founder Reed Hastings gave up on his position as CEO, the company has taken a different direction altogether with its strategy on password-sharing and also advertising focus.

As a result of its curb strategy on password-sharing and tiered pricing, the company has done extremely well in the streaming front with many more net subscriber growth, but they are about to change this key metric which they have been tracking for so many years into hours of engagement from subscribers instead.

They felt that the more the subscribers and users are engaged by staying in Netflix ecosystem longer, either through watching movies or playing games, the more opportunities the company can extract from its users, e.g through advertising as it can result in higher revenue drive.

In its own words, it says:

“Viewing is key to Netflix’s success. It’s the best proxy we have for member happiness, and when people

watch more, they stick around longer (retention), talk about Netflix more often (which drives acquisition)

and place a higher value on our service.”

Advertising is the New Revenue Driver Growth

The online streaming has been a game-changer for the entire industry as many individuals move from the traditional TV and DVDs to streaming. This move has been accelerated by Covid with more people staying at home with nothing to do but to spend more time on online streaming.

For decades, Netflix has been competing in the streaming war era with companies such as Disney+, Paramount, Warner Bros, Comcast. This is all about to change now, with the company taking on the directional path towards digital advertising as its next growth area.

In digital advertising, the landscape is a lot more complex and challenging.

It is now fighting with the same space with the likes of Amazon, Google, Meta, and Tik-Tok. Netflix would have to prove to advertisers that its appeal into the space is as strong, if not better, than the likes of YouTube or Instagram.

Netflix Q2 Earnings Summary:

Overall, the company announced earnings for Q2 which we knew was strong, yet expected, as paid net member growth and churn was once again the focus for discussion.

Paid net adds in the quarter was primarily driven by strong acquisition and healthy retentions as the company demonstrated positive net additions across all regions.

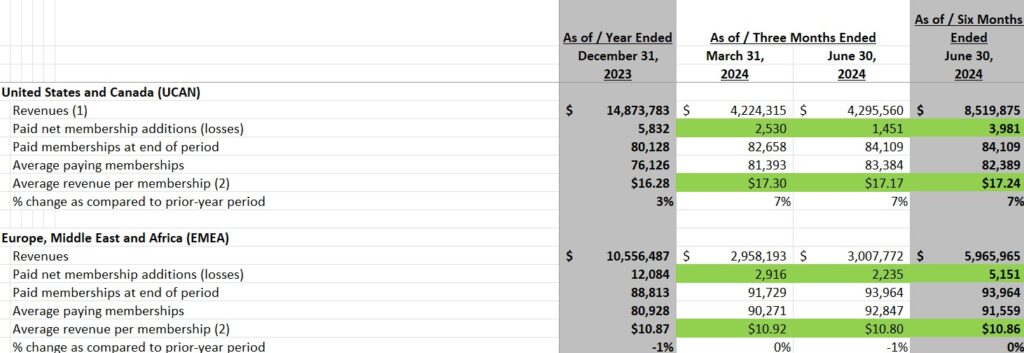

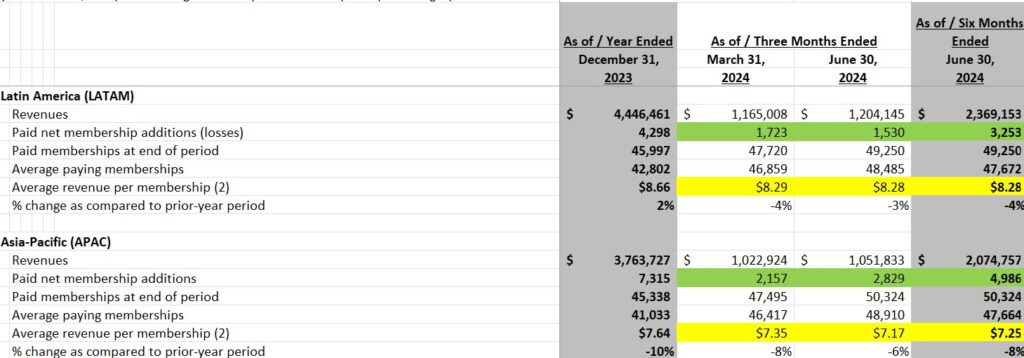

Revenues grew 17% to $9.6 billion, slightly beating expectations of $9.5 billion, largely on the back of user growth. Overall Paid memberships rose 16.5% on average to 277.65 million globally (net adds of 8.05 million).

Meanwhile, average revenue per membership ticked up just 1% (5% on an F/X-neutral basis). Those exchange differences were again linked largely to heavy devaluation of the Argentine peso in Latin America region relative to the dollar.

Meanwhile, operating income rose 42% year-over-year to $2.6 billion, and operating margin improved by nearly five percentage points, to 27.2%.

Earnings per share rose 48% and also topped expectations.

Growing margins was also one of the executives’ primary focus as they are now targeting 26% operating margin, up from 25% prior before.

Apart from the US and Canada region which shows a higher growth in Average Revenue per membership, all the other regions are either flat or drop from the last FY24 ended Dec.

While Netflix continue to reiterate its full-year forecast for $6 billion in free cash flow, this particular quarter it fell short of expectations by just generating $1.2 billion instead of the expected $1.6 billion, but management attributed this due to timing factor more than anything else.

Valuation

Netflix is an “expensive” stock, but look at it from a growth point of view because it sports a growth stock valuation.

At $650 per share, it is trading at ~41x TTM PE and approximately ~36x FWD PE multiples.

Revenue growth is expected to be in between 15-20% in FY2024, and then subdued slightly lower to an average of about 15% or less over the next few years.

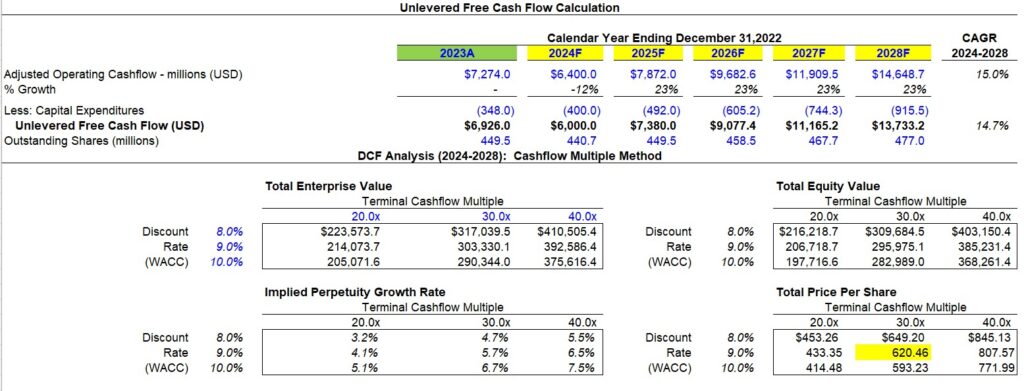

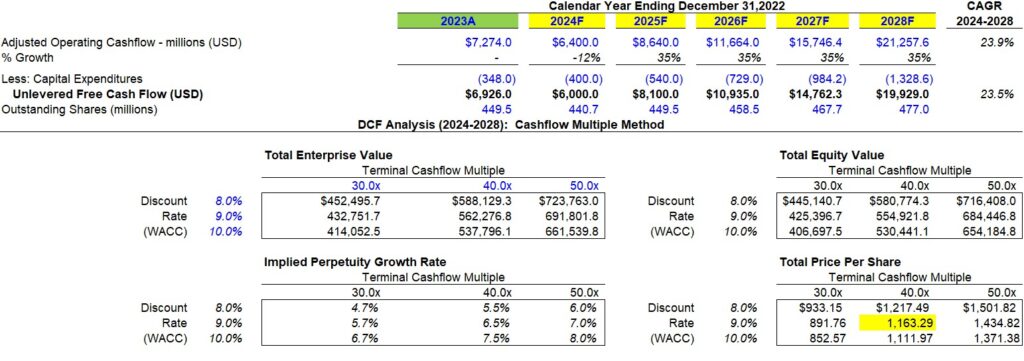

TTM Free Cash Flow is at $6.9 billion, and management reiterated forward FCF to be around $6 billion for the full year.

TTM Capex has averaged at around $300-400 million per financial year without taking acquisitions into account.

If we value Netflix to grow its free cash flow at 15% CAGR over the next 5 years, at a decent EV/Cashflow multiple of 30x, we get an intrinsic value of $620, which is just about fairly priced in now.

However, if we assume a more bullish scenario for Netflix, say with the likes of these higher performing metrics:

- Higher Operating Margin of above 26%

- Higher dominance of the streaming market through continuation of positive net subscriber additions (i.e growing by more than 15% CAGR)

- Digital advertising takes off with ad-supported subscription plans grow from $6 billion in 2023 to $21 billion by 2028.

If we do that and put the assumptions back into our model, and then apply the higher multiples of 40x EV / Cashflow, then Netflix intrinsic value could be worth north of $1,163.

Again, at this point, a lot is pretty much based on execution and how much management can stir off the stiff competition from its peers.

Follow me, if you have not, on my social media channel here!