This article was written and first appeared on Fundflicks – Hongkong Land Holdings Limited (SGX: H78): Too Cheap to Ignore (fundflicks.net)

The ongoing saga surrounding China’s largest private property developer – Country Garden Holdings, who failed to pay coupons on the bonds due 6 August 2023, has exacerbated the fear on the property cashflow situation – keeping investors on the tenterhooks on the industry latest situation.

This adds on fuel to another already-done embattled Chinese property developer Evergrande which has taken the market by the storm with each passing day.

Because of that, it is no surprising that when you combine property together with the word Hongkong or China, investors would shun immediately right through it.

In this article, we’ll explore why Hongkong Land is different from the others and why investors should consider this undervalued gem.

Introduction to Hongkong Land:

Hongkong Land is a major listed property investment, management, and development group.

Founded in 1889, Hongkong Land’s business is built on excellence, integrity and partnership.

The Group owns and manages more than 850,000 square metres of prime office and luxury retail assets in key Asian cities, primarily Hongkong, Singapore, Beijing, and Jakarta.

The Group’s Central Hongkong portfolio represents more than half – 450,000 square metres of prime property. It has a further 165,000 square metres of prestigious office space in Singapore mainly held through joint ventures.

Below is a snapshot of all their investment properties, primarily in Hongkong, Macau, and Beijing.

Hongkong Land Holdings Limited is incorporated in Bermuda and has a primary listing in the London Stock Exchange, with secondary listings in Bermuda and Singapore.

Company Fundamentals and Financials:

Since announcing a significant share buyback program, the company has spent over US$600 million since September 2021 in share buybacks.

The move brought about some cheers and support to the underlying share price for a while but since pulling back on the moderation in the buyback since this year, the share price performance has again languished low and dipped as a result.

In the latest 1H 2023 earnings announcement, the Group’s Central office portfolio in Hongkong delivered a solid performance amidst challenging market conditions both locally and globally.

While physical and committed vacancy increased to 6.9% and 6.2% respectively at the end of Jun 2023 (which was an increase from 4.9% and 4.7% at the end of 2022), it was still lower than the average vacancy in the other Central market.

Negative rental reversions also occurred this quarter – decreasing average office rents to HK$107 p.s.f, as compared to HK$111 in the same period in previous FY.

The Group’s LANDMARK retail portfolio delivered an improved performance during the first half of 2023 – with increase in tenant sales and removal of temporary rent relief led to an increase in average retail rent to HK$204 p.s.f, as compared to HK$181 in the same period previous FY. The LANDMARK retail portfolio also remains effectively fully let.

In Singapore, committed vacancy across the Group’s office portfolio dipped to 1%, with positive coming in from rental reversions average rents up to S$10.9 p.s.f, as compared to S$10.6 p.s.f in the same period previous FY.

On the sale of development properties, the performance and profit contribution resulting from this has dipped as there were significantly lower number of planned sales completions in this FY.

The weak economic outlook in China in particular, has weighed down on consumer sentiments towards purchasing a development – despite the introduction of policy support measures rolled out by the central government.

The Group’s attributable interest in contracted sales was US$745m in this 1H 2023, as compared to US$881m in the same period last year.

In Singapore, the Group continued to recognize profits on the percentage of completion basis, which was broadly unchanged from the same period last year.

Market conditions remained healthy, with strong sales at the 638-unit Tembusu Grand project, which was 55% sold at the end of Jun 2023. The Group’s attributable interest in contracted sales was US$487m, as compared to US$345m in the same period last year.

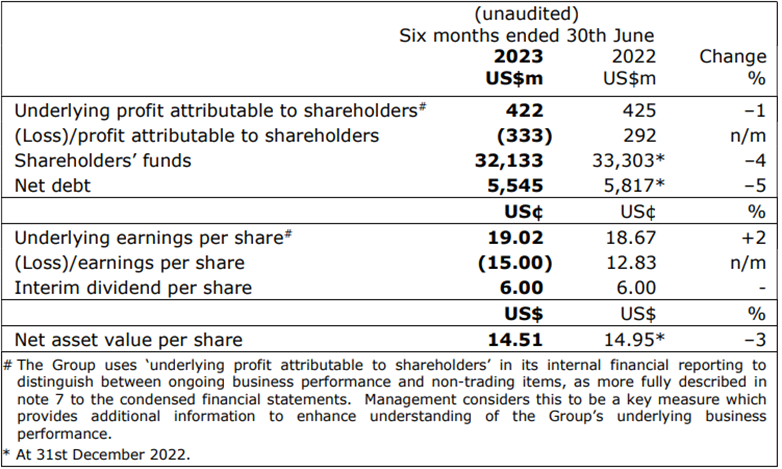

Overall, underlying profit performance attributable to shareholders was US$422m, which was comparable to the previous financial year of US$425m.

Underlying EPS has grown slightly by 2% from 18.67 cents to 19.02 cents in this 1H 2023.

There were unrealized losses arising from the Investment properties revaluations in this 1H of US$755m, which was mostly attributable to the Hongkong investment office portfolio as a result of slight decrease in market rents and a cap rate expansion.

As a result of the fair value losses on investment, the Group reported a “loss” attributable to shareholders of US$(333m) for the 1H 2023. This resulted in a slight drop in the Net Asset Value (NAV) of US$14.51 per share.

Too Cheap to Ignore:

Net-net is a value investing technique which was early in the days emphasized by the great investor Benjamin Graham – in which a company’s stock value is valued and determined by the net current value of its assets.

This technique focuses on balance sheet items, such as current assets like cash, investment properties, accounts receivables, less liabilities and any doubtful accounts.

The reason why this focuses so much on balance sheet rather than earnings is because it is a much reliable to rely on balance sheet than earnings, which tend to fluctuate depending on many factors such as business cycle, recognition of revenue method, and seasonality.

Balance sheet, on the other hand, is much more durable and easily verifiable whereas earnings are more subjective in nature.

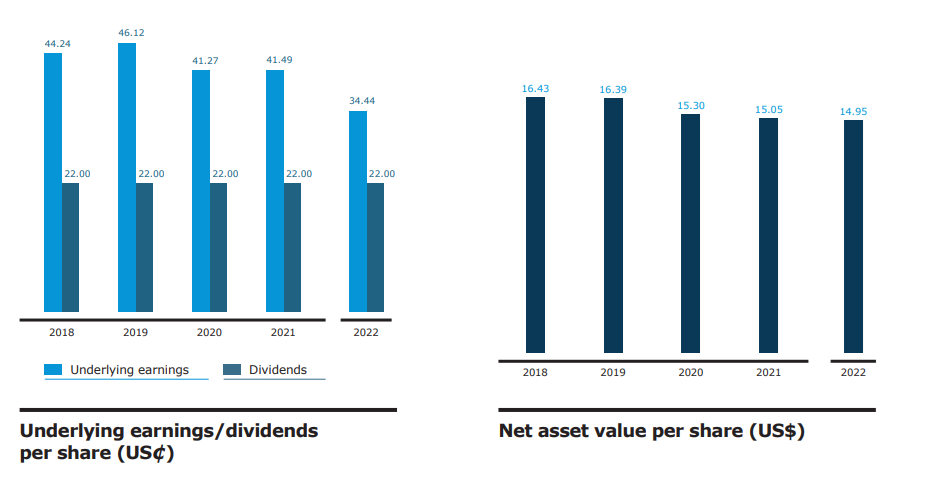

Based on HK land long track record, you can see that the company has been generating strong underlying earnings and issuing constant stable DPU over the years.

Net asset value has over the years also increased over time, albeit the last few years because of situation in HK such as riot, Covid, and weak economic impact has impacted the outlook of the rents quite a bit.

At the current share price of USD 3.54, investors are buying this undervalued piece of the company at 6.2% yield (at 22 cents DPU) while waiting for the company to recover and close the gap to its net asset value of the company, which as of 30 Jun 2023 is valued at USD 14.5.

This gives investors buying at an undervalue piece at Price to Book ratio of only 0.24x, which is incredibly cheap as compared to some of the other property developers listed in HK.

Even if the company offers no further upside, investors would break even on the stock in about 16 years just through the dividends alone (assuming they are maintaining their 22 cents DPU every year).

Given that the company is over 100 years old, have generational years of experience, and cashflow machine, I think this could be a safe bet for those looking to expose in the industry sector.

But hongkong land is cheap for a long time. The share price declined even before evergrande. Why do you think that now is a good opportunity to buy?

I think link reit looks way more attractive. What do you think?