One of the most favourite pastimes for economists, analysts and investors alike in the early part of the year is to make market prediction on where the stock market will be heading.

Ipsos Global ran a similar survey and research report on the outlook of 2023, including where the economy and stock market is heading as well as market sentiments. If you’d like to view the full report, you can read them on your own in the link inserted above.

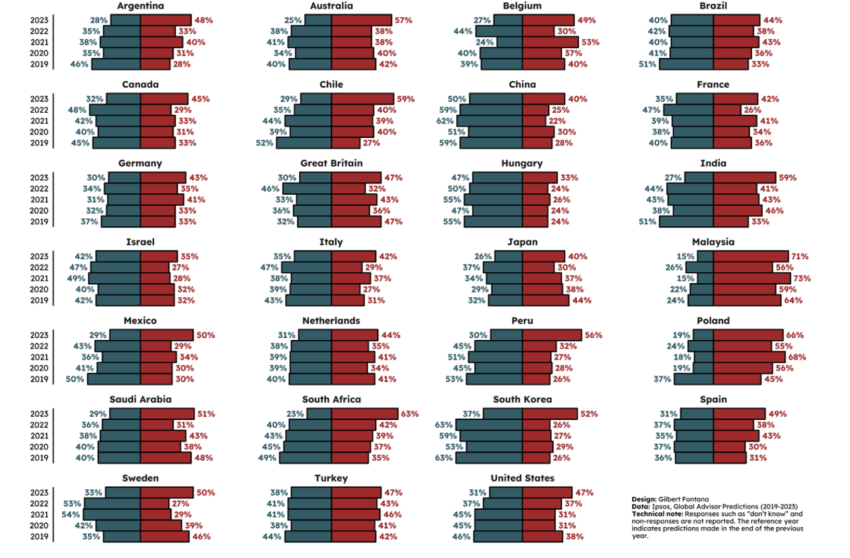

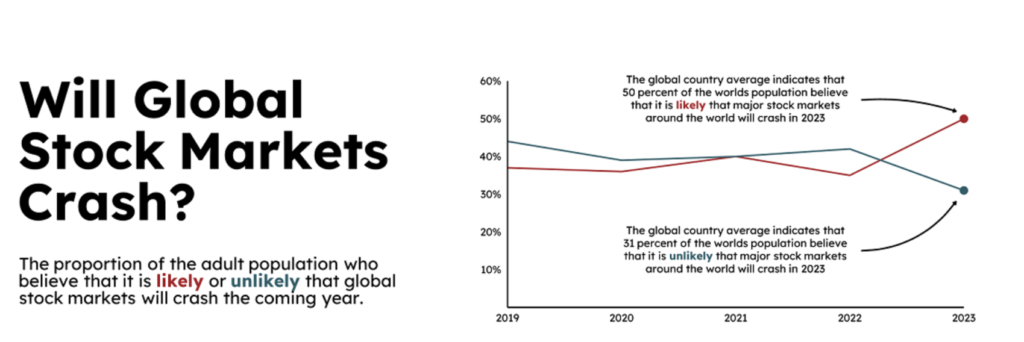

The survey highlights the proportion of the adult population taken from more than 24,000 adults across 36 nations on their beliefs of where the market will be heading in 2023. As you can see from the summarized graph below, the sentiments pointing toward a market crash in 2023 slopes upward and these people believe that the market is “likely” to crash after experiencing a tough year in 2022.

This is a detailed breakdown by per country basis – where red bars are indication of market to “likely” crash.

Now, if you ask your circle of friends or colleagues, many are probably going to tell you the same.

We’ve seen companies struggling with the declining growth and margin erosions while the majority of companies who flourish in the year leading to post-pandemic are starting to cut jobs due to over-capacity and declining demand. In fact, as I was writing this article, Microsoft has just released its latest earnings and outlook which paints a rather gloomy and muted growth for the rest of the year. Google and Amazon have also announced job cuts as with the many companies who suffered from over-capacity.

The outlook at least for the first half of the year is likely to be gloomy.

The interesting part about this is although many believes that we will be getting a gloomy hard landing at least in the 1H of the year, the same people (including the economists) also believe that we are likely to return back to growth in late 2023, if not in the early part of 2024. From a timeline perspective, that isn’t too long and herd beliefs like this may just become more prominent and tempts you to adjust your portfolio.

But is it really necessary?

Should You Market Time or Continue To DCA?

Perhaps the million-dollar question here is since it is likely that we are heading into at least a soft landing (if not albeit a hard landing scenario) in the US and Europe economy, should you be adjusting your position by selling into the market and then buying back again in the 2H of the year when Fed pivots are confirmed.

Or will you end up better just DCA-ing into the market and staying invested throughout.

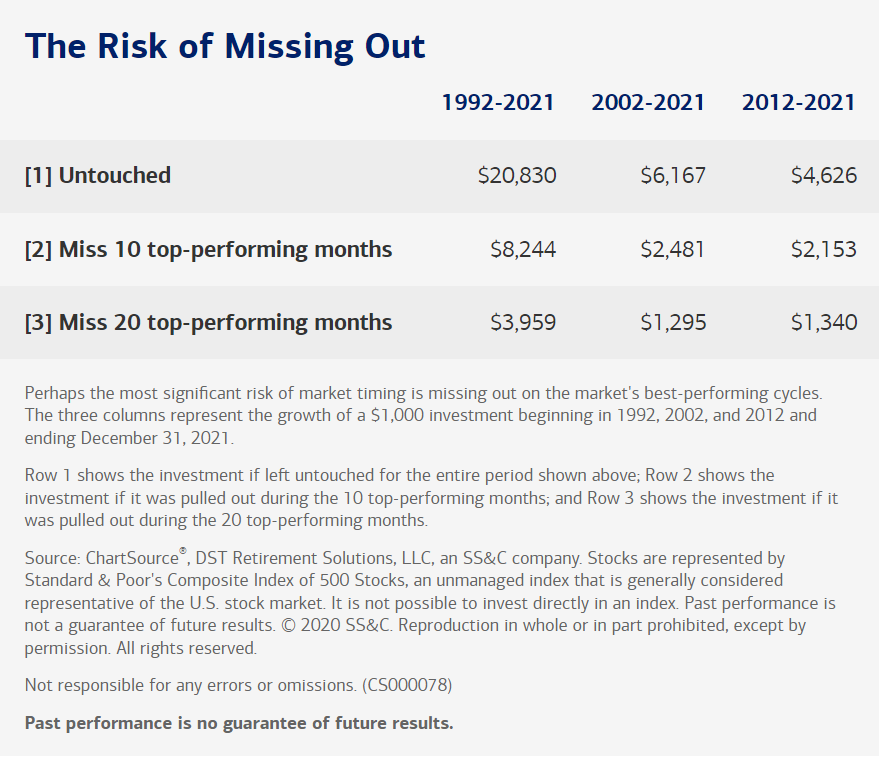

According to Merryl Lynch, the most significant risk of market timing is missing out on the market’s best-performing cycles and investors are likely reeling being left out of the eventual start to the bull market when it does. For instance, if you miss the top 10 performing months throughout the 30-year period from 1992 to 2021, your portfolio return would have performed less than half than if you have left it untouched.

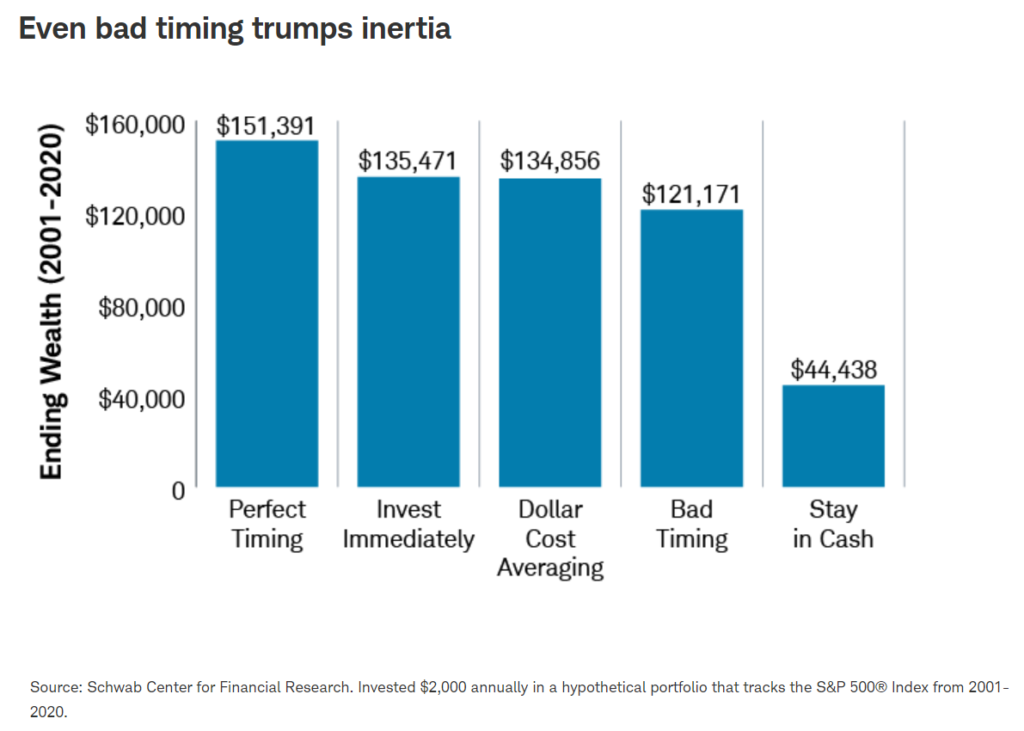

Charles Schwab also ran a test for all 76 rolling 20-year periods dating back to 1926 (e.g 1926-1945, 1927-1946, etc) and in 66 of the 76 periods being analysed, the data returns the same as per below ranking.

Rank 1 – Perfect Timer

The perfect timer is someone who technically doesn’t exist in the real world but let’s assume for the sake of the experiment this person does. The perfect market timer was able to place his investment at the lowest closing point of the market every year (e.g invested during Sep 2001 bottom and then again in Oct 2002 bottom of the year). After allocating $40,000 in 20 years period ($2,000 for every bottom year x 20 years), the perfect market timer would have seen his portfolio grows from $40,000 to $151,391 – giving him a solid 378% return).

Rank 2 & 3 – Invest Immediately and DCA

The concept of the investing immediately and consistently works almost the same way except with investing immediately this person starts to put it at the start of every year (i.e 2 Jan xxxx), while the DCA would divide it across 12 equal months.

I’d say this is probably the closest to what most people are doing including myself as we receive our income or salary on the same interval every month.

Based on this experiment, you can see that after 20 years, the portfolio would grow from $40,000 to about $134,000-$135,000 – which gives still a solid 338% return.

You can see that the return lags the perfect market timer, but the amount of pressure needed to time the market perfectly is vastly different. Plus, it is much more realistic for an average investor to use this strategy in this case than someone who tries to market time.

Rank 4 – Bad Timer

Assuming you are someone who is truly bad at market timing, and whenever you tried to put your money, you ended up investing at the peak month of every year (e.g Jan 2001) throughout the 20-year period – you might think that your return would have underperformed by a lot but based on the experiment ran from Charles Schwab, it is not the case.

This experiment shows that you are likely to still sit in the handsome territory as long as you are consistent in your approach – and you are likely to end your portfolio with $121,171, which still gives you a decent 303% return).

Rank 5 – Stay in Cash

Needless to say, someone who has consistently stayed in cash or T-bills earning minimum risk-free rate returns across the 20-year period would have severely underperformed the rest by ending the year with only $44,438, which is a 11.1% return across 20 years due to persistently low interest rate (it should be doing better during this time with interest going back up).

Conclusion

Investing is part-mental and emotions at the end of the day.

As much as we can, I think we should try to minimize the impact of it since it is something which humans are not very smart to be able to control it effectively.

But yet many are still looking to time the bottom of the market when realistically it is much easier to just allocate your capital consistently every month.

Maybe the past 20-30 years are not indicative of what the future performance is going to be like, but we’ll also know that it is unlikely for most people to comfortably time the market.

What do you think? I want to hear your thoughts.

If you have not followed my social channels, you may want to do so as I frequently post ideas and thoughts in those channels so if you are interested, you may follow me at my Facebook, Instagram or Twitter profile here.

B,

I’m tickled pink 😉

Just to Trust but Verfiy, do you voluntarily contribute to CPF?

Hi Jared

No, I don’t voluntarily contribute to CPF after many many years.

dca will not work for nikkei index. what if us stock index behave like the nikkei for the next 20 years?

Hi David

If stock index behaves like Nikkei of the past, then individual stock picking is screwed too either way.