I wanted to quickly run through my thoughts on the Tencent latest Q3 earnings announced yesterday.

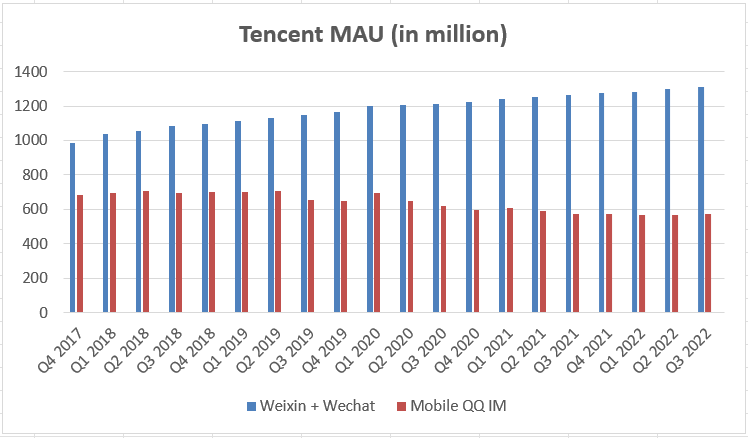

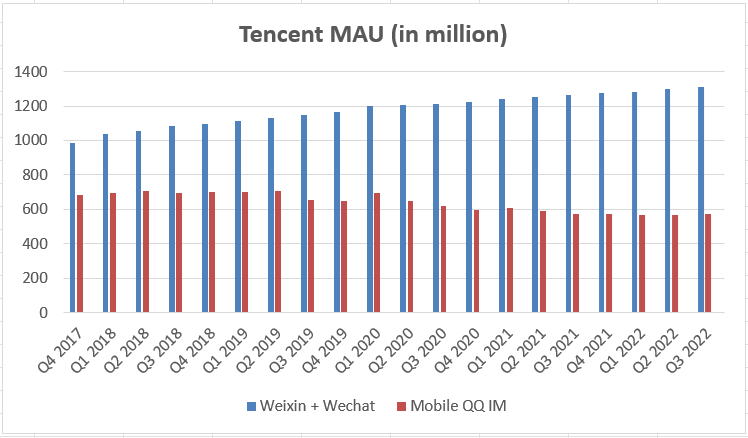

First up, operating metrics MAU is still up year on year and quarter on quarter for both Weixin + Wechat as well as Mobile QQ but as you can see, they are approaching the matured 1.3b numbers so inevitably growth is slowing down on this front.

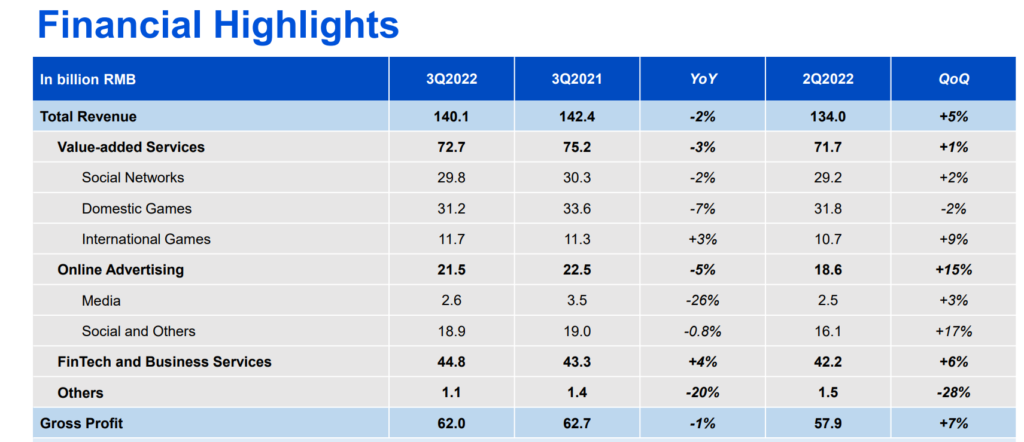

Overall numbers seem to be decent, with many sub-business units registering quarter on quarter increase.

In particular, what was particular interest for shareholders is the domestic games segment – major titles like Honour of Kings and Peacekeeper Elite saw a decrease in revenue as a result of the stringent minor protection measures. However, judging by its quarter-on-quarter comparison, it appears things might have bottomed. Sea Ltd recent gaming results also indicated a bottom signal for its gaming segment in terms of falling PAU users.

Online advertising revenue declined 5% year on year to RMB 21.5b in 3Q22, which is a vast improvement than the Q2 year on year decline of 18%.

This improvement is boosted by the eCommerce and FMCG categories which continues to outperform in this difficult year.

Fintech and business segment continues to perform strongly as expected.

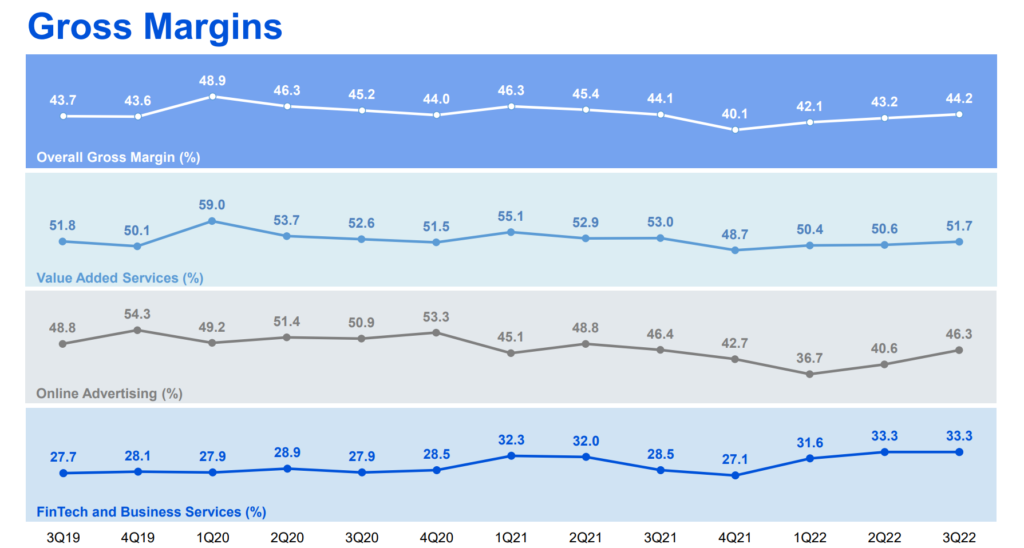

From a margin’s perspective, the overall margin remains healthy at 44.2%, driven by increase in every business unit. You can see that the margins for online advertising took a dip back in Q1 and Q2, but it has now quickly resume back to the previous year of Q321.

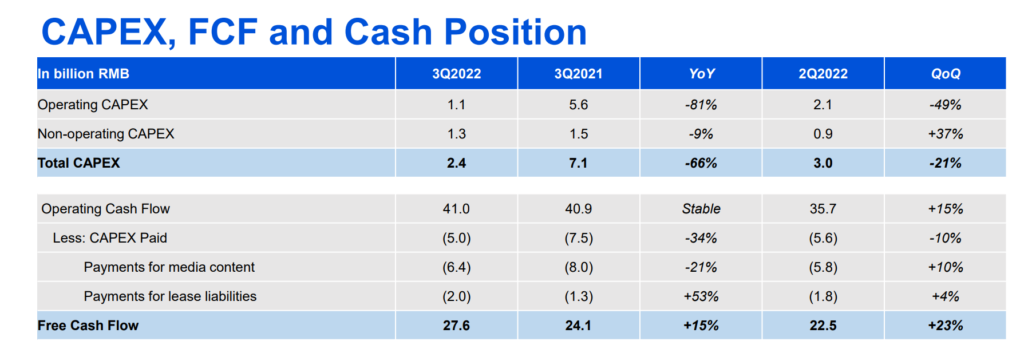

From a free cash flow perspective, it has remained stable year on year as the company goes on to reduce capex spend as well as slowing down the cost of marketing and other spend.

The company has been repurchasing and buying back its shares aggressively for the past few quarters (~42.8m shares costing RMB11.8b during Q322) but at some point, they will stop doing it aggressively once the share price resumes back normal.

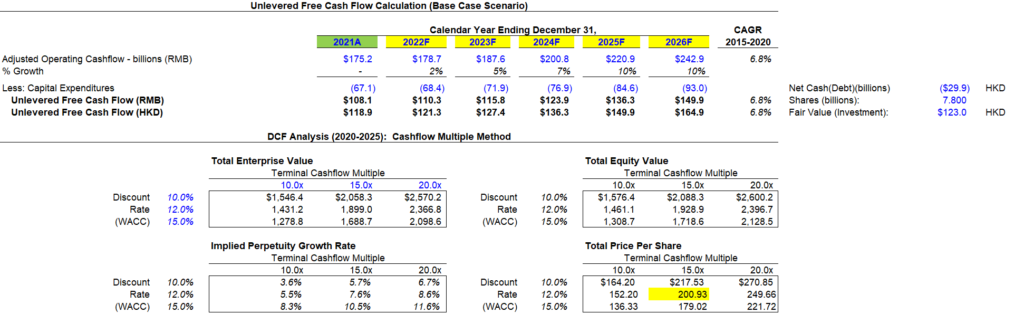

DCF Valuation Model + Fair Valuation Investment

As of 30 Sep 2022, the Fair Value of the shareholdings in listed investee companies, excluding subsidiaries, stand at RMB532b, and the carrying value of the unlisted investee companies stand at RMB340b. Together, they made up RMB 872b.

If we translate this to HKD/share, it is approximately worth HKD123 (RMB 872b x 1.1 / 7.8 billion outstanding shares).

Based on today’s base / weak case bleak scenario, I am projecting a flat 2022 comparison, and a single digit incremental growth over the next 3 years before it stops at 10%. I do think that as an innovative company they can do much better than this, but I wanted to see how much I get from this model.

It appears that we get an intrinsic value of HKD200 for its core business at a multiple of 15x, which is still conservatively -1SD away from the last 5 years mean. Adding this with the fair value of its investment, we will get an overall intrinsic value for the company at HKD200 + HKD123 = HKD323.

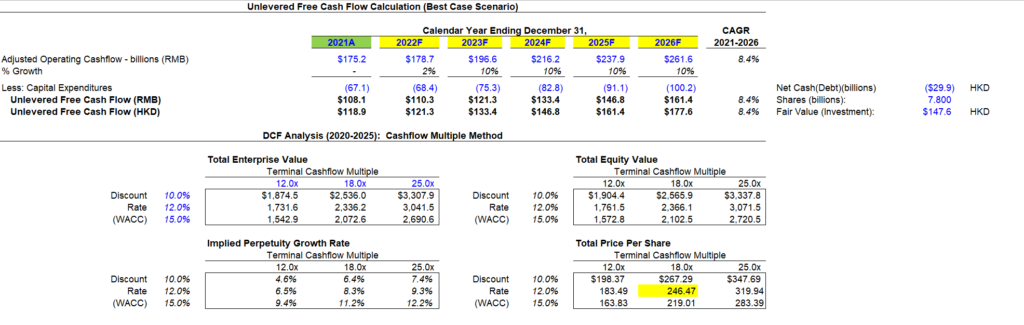

The gaming licence approval especially for domestic is a big driver catalyst for its intrinsic value to move up. Assuming this happens over time and the economy gets better over time, online advertising and cloud should continue to grow double digit. In this regard, I am revising my model into a more optimistic scenario below.

The terminal growth is now changed to 10% and multiple to go up to 18x.

On fair value of investment, I have also bumped it up by 20% upwards.

This model would return us an intrinsic value of HKD 246 + HKD 147 = HKD393.

Obviously, if the company can do better than this, then its value is worth even more.

Final Thoughts

Tencent has been dishing out special dividends for two years in a row now.

Last year it gave out its JD shares and today they are giving out Meituan shares, which translates to about 5.5% yield. For 2,500 shares, I will get 250 of Meituan shares which is worth around SGD8k today, so not bad at all!

The company seems to be moving in the direction of overseas growth and they have been excellent capital allocator so things might just move from there for us to monitor further.

Is the no. of shares outstanding correct? Should be 9+bil instead?