By the end of next week, I will be heading to Europe with my family for our year-end holiday where we will be spending about 4 weeks. Thereafter, I will be heading back home to see my parents until the end of this year so this could very well be my very last post this year (*If I still have some time, I’ll cover one or two earnings results for some of the Chinese companies I own next week).

Some big changes this month so I wanted to execute in earlier and be done with purchase for the rest of this year before I go for my trip.

A couple of months ago, I mentioned that I was waiting for my funds for the proceeds from the sale of our home.

I was expecting for it to come slightly later at the beginning of next year, but the option to exercise and completion came in much earlier, so we received the funds in earlier too as a result.

While it was never a deliberate conscious timing decision, it was nice seeing the funds hit the account while we are still in the midst of a bear market.

I began executing by purchasing some shares which has been in my radar for some time, in particular increasing my allocation to US stocks in general.

I also wanted to clear my leverage and margin accounts for a while so voila, I am now clear on any leverage play.

This will be a slightly longer portfolio updates than usual so bear with me.

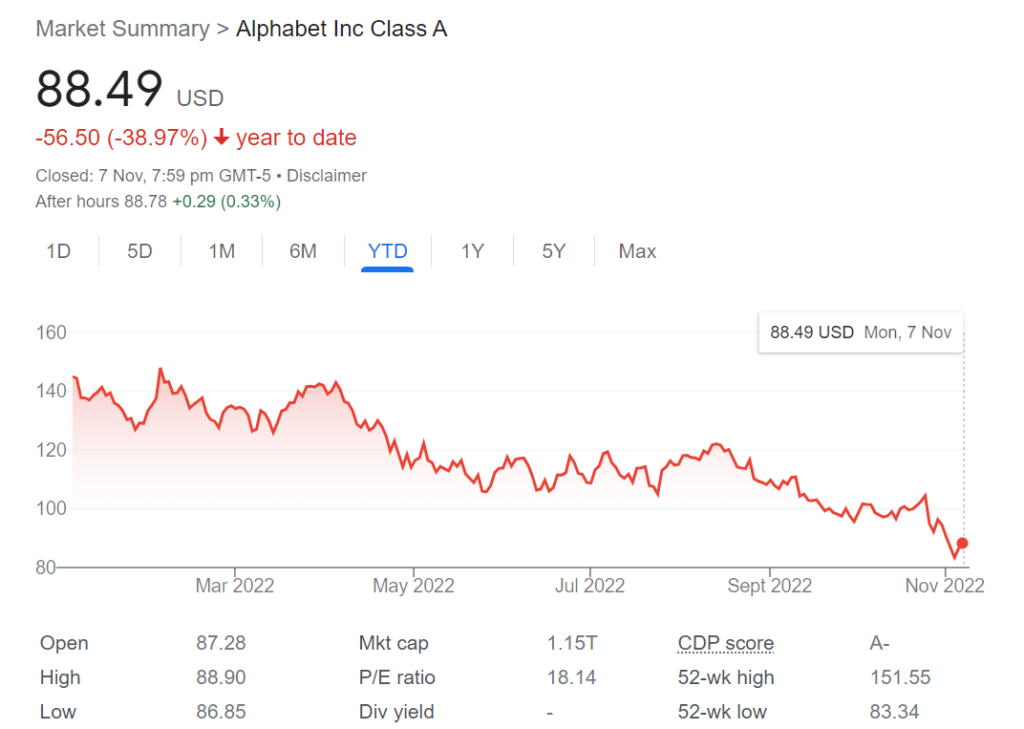

The biggest purchase I have made with the funds by far this year is on Alphabet (Nasdaq: GOOGL).

Alphabet is one FAANGS company which has not done so well this year – it has dropped ~39% YTD from where it was at the beginning of this year, and it was definitely not a reflective of what they are worth for, despite some business challenges they face.

From a valuation point of view, Alphabet currently sits somewhere in the middle of the other FAANGS – not as “cheap” as Meta but it is also not as expensive as Apple or Amazon. More importantly however, they have a business moat which I think is here to last for a lot longer.

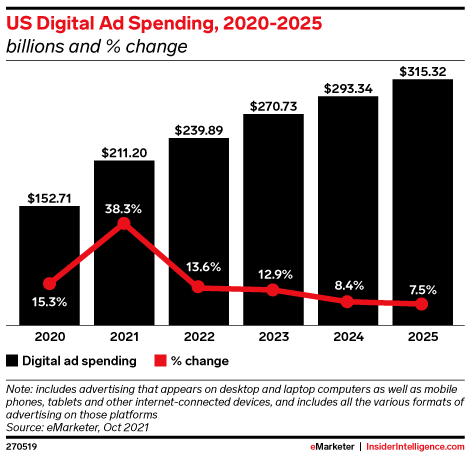

While digital advertising is undoubtedly slowing this year due to macro-economic factor, ads spent is still expected to grow at a compounded annual rate of 11% until 2025 so with Alphabet it is a direct beneficiary when things turn around eventually.

Furthermore, Google Cloud is also expected to break-even by later 2025 and is still a fast growing 26% CAGR business, which should produce tons of cashflow by then to be able to sustain and grow on its own.

Overall, I see this as a longer-term position, and a proxy to the US exposures and S&P as a whole, and returns should track a closely correlated return over time with the S&P.

My second largest purchase is doubling my positions on Alibaba (NYSE: Baba).

I wrote an article back on the 24th of Oct journaling the capitulation days of Chinese stocks just two weeks back and while I have not been able to “catch” the bottom, at current price it does still represent a good value to wait for the eventual China recovery to come.

This is a bold move and one which certainly does not fit into one’s risk appetite easily so take everything I say with a pinch of salt. If you are more comfortable investing when the mood is lifted, just stay out of it until this entire bear market is over.

For me, I’ve always wanted to accumulate into positions in a bear market as I believe the risk reward tilts to favour when things turn around eventually, but this will take some heavy stomach to swallow. Going to a holiday and looking away from the daily price movement of the market might work, so that is what I will do very soon.

Other than these two big purchases, I’ve also added a couple of smaller positions in both US and HK Tech stocks.

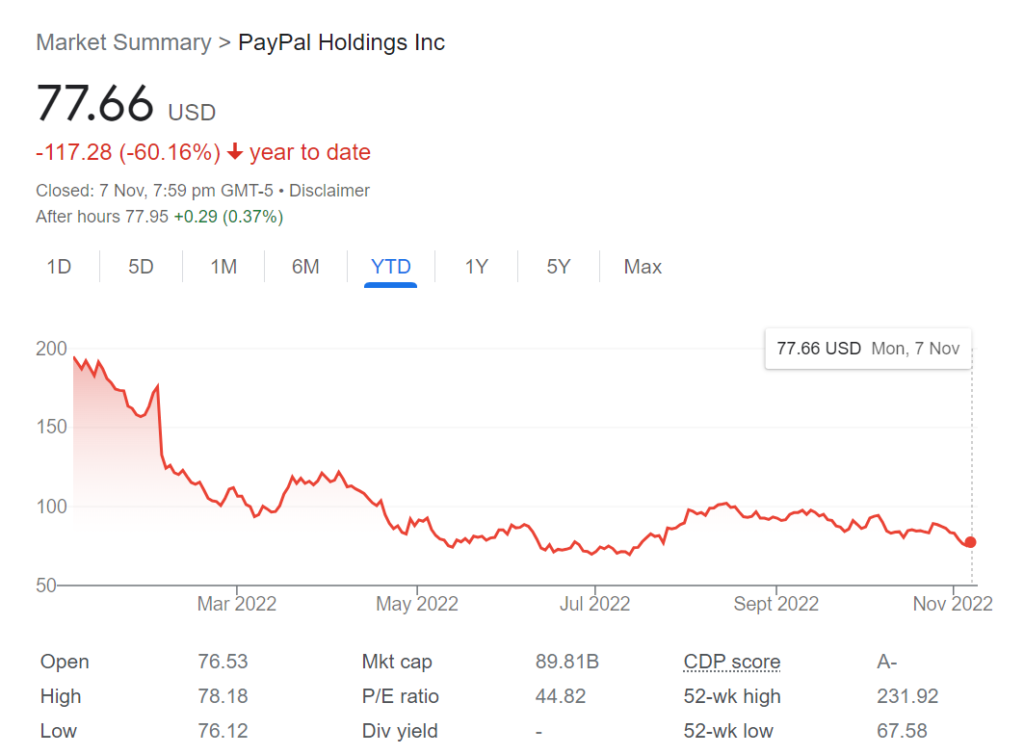

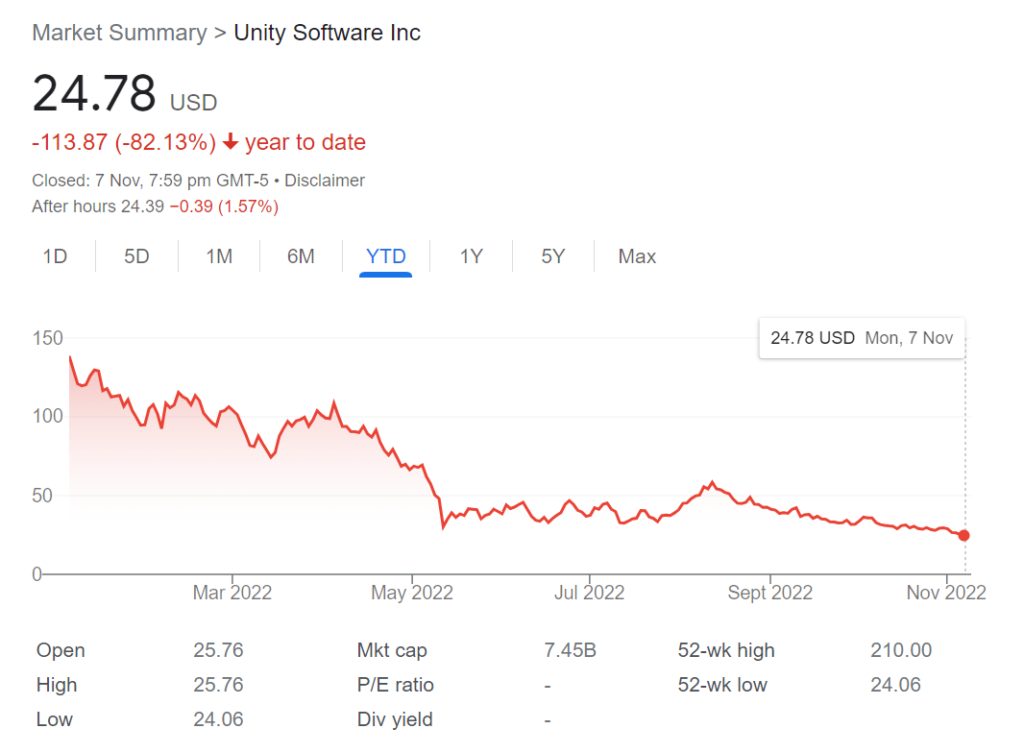

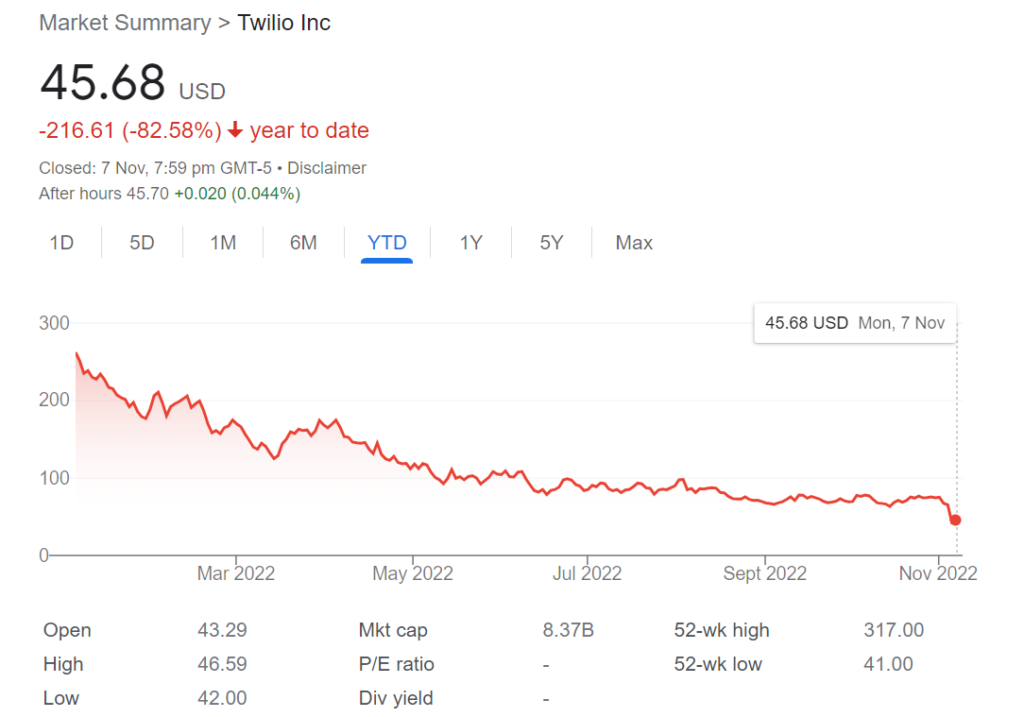

I added a new position for PayPal and Unity, and accumulated more positions for Twilio, Tencent and HK Tech ETF.

Let’s first revisit PayPal – it is another company which I think is in a deep value territory and I have covered this company much earlier in the months. Since then, it has further gone down south even more with the broader market decline.

Year to date, the company has retreated by about 60% and has just released its latest earnings last week, which actually doesn’t fare too badly.

The problem is – like most companies providing guidance for next quarter – is that PayPal guided for a weak Q4 outlook as we are approaching the holiday season as the company expects e-commerce spending to be sluggish globally, especially in the US. This is not surprising given the same outlook given by many other e-commerce companies facing the same macro-outlook.

With normalized earnings at about 16x, this is lower than the usual average of FCF multiple of about 20-30x so much will be seen on future reversion to mean if the company can get back on track post this difficult outlook. While there are many competitors around, PayPal still have a very big part to play in the fintech payment ecosystem.

For Unity, this is a starting smaller position and a company I have always been interested since the last two years but has never been able to buy due to its lofty valuation.

The company has retreated by about 82% this year and valuations are starting to get attractive again.

A big part of the thesis for investing in Unity is the company’s unique proposition in different verticals – the latest being outside of its core gaming business. The recent Weta Digital acquisition is an example of how they are diversifying yet strengthening their other core verticals within the visual effect of a movie industry.

With its Q3 earnings soon coming this week, will see how they will fare going forward.

On Twilio – this is a deeply wounded company after dropping massively on the most recent earnings just last week. To date, it has retreated by about 84% from the beginning of this year.

At its peak, valuation was very rich and at some point, we know that the company’s valuation was never going to be sustained as it hit 42x Price to Sales when it was at its peak of $435 last year. Since then, the broader market decline and challenges in the economy led to slower growth, which it has demonstrated over the past 4 quarters.

My entry price for Twilio at $150 proved to be equally fatal as I paid the price for still paying too high back then at about 10x sales. At today’s price of $45 however, it represented what I think is a good valuation at Price to Sales of 3x, with the company aiming to breakeven by GAAP EBITDA by 2024.

Like most companies, Twilio also lowered its revenue guidance for Q4, but I think the longer-term prospects are bright for this CaaS company.

The company continues to generate healthy organic growth and net dollar expansion and I can see them being around for much longer years in the future.

The tailwind risk with this company is also because they are largely focusing on their cashflow and profitability, they might have to be selective with their choice of projects to run and this will likely impact the short-term growth rate.

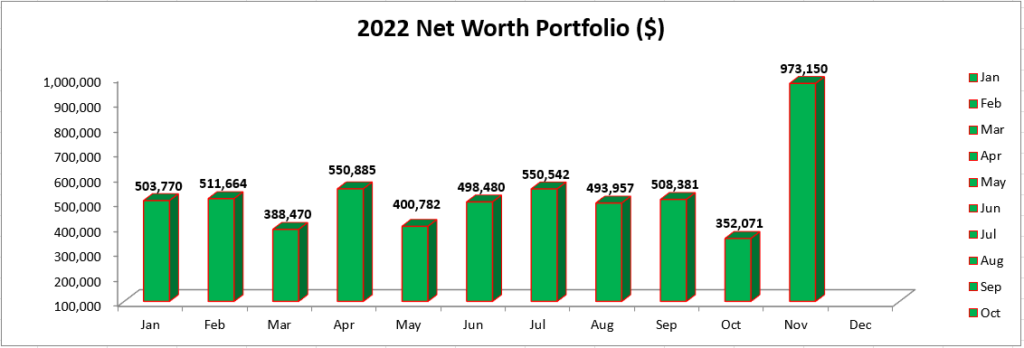

Networth

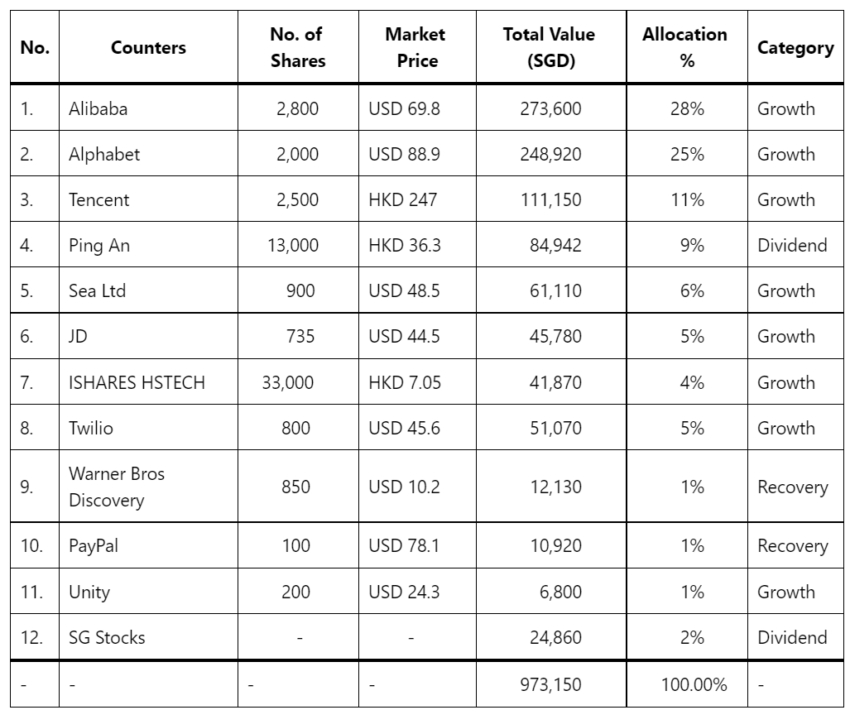

This has been a long post, so I’ll quickly summarize the increase in the equity positions to the portfolio.

All in all, I added about roughly just under half a mill dollars’ worth of stocks to the Nov portfolio, and also cleared about $180k worth of margin leverage.

This also marks the last purchase I will be doing for this year, and possible also the last article posts of this year (we’ll see on this part).

I will continue to dollar cost average and accumulate more undervalued positions started beginning of next year with my monthly routine.

To the rest of readers, this has been a tough year for investing but if you can past this stage, future years are going to be better. See you guys soon in 2023!

If you have not followed my social channels, you may want to do so as I frequently post ideas and thoughts in those channels so if you are interested, you may follow me at my Facebook, Instagram or Twitter profile here.

Hi B,

Good to hear from you again.

Can i check out of $973,150. How much is your total capital from salary or other part of earning (excluding any profit from stocks/dividend)?

Thanks & Regards

Peter

Wow Brian u have balls of steel. What is your new average cost for Alibaba now?

which HK tech etf counter did you buy?

whats the rationale for this particular etf? since all the rest of the stocks in your portfolio are all single stocks?

Hi Brian,

Wah seh. You could be taking a lot of risk. What if China taking back Taiwan by force?

Regards,

Gerald

https://sgwealthbuilder.com

u sold yr house and cash out 200k+ profit but your portfolio went up by 500-600k? some things dont add up leh

as you already said, it is profit. When you sell a house, you cash out your equity portion (capital + profit).

i assumed the capital goes into the payment of yr current house.