I felt the need to address this because there were so many who messaged me yesterday about potentially one of the most turbulent capitulation investors investing in China and HK stocks face this year and judging by the number of messages and concerns, it is probably safe to say that it is capitulation.

Most of you would have known my portfolio composition by now so it is safe to say that I was probably hit by a mile more than whatever you have in your portfolio (unless of course you have a higher allocation than myself).

Many of the messages I received were asking basically on the same common theme and that is if I am concerned about the heavy sell-off yesterday.

I think we have to look at this from the two lenses – one the stock price drop and another the qualitative angle of the committee leadership round-up from the National Congress.

Let’s address the first concern – the stock price drop.

Yesterday on the 24th of Oct 2022, many of the China companies (not just limited to tech) suffered heavy losses and from the way it dropped it is quite certain that it is capitulation at bay. I have a few friends who have managed to cut loss and limit their losses, while others were forced in order to stay afloat on the margin side.

The good news about capitulation and despair is that we are likely nearer to the end than the beginning, and as with most things, the bottom should already be near (again for context, I’m not saying necessarily yesterday was the bottom, but you get the idea). When things have stabilized and there are no more sellers, then we have that start of the uptrend. So, we just have to be patient reinforced.

I’ll hold my Tencent and Baba stocks to zero if I have to, but this is just to reinforce my conviction in these companies, and I have the patience to do so.

Sure, growth might have come down, and risk premium might have gone up, but even with these two combined, I am still seeing enough risk reward in my favour at the moment to hold.

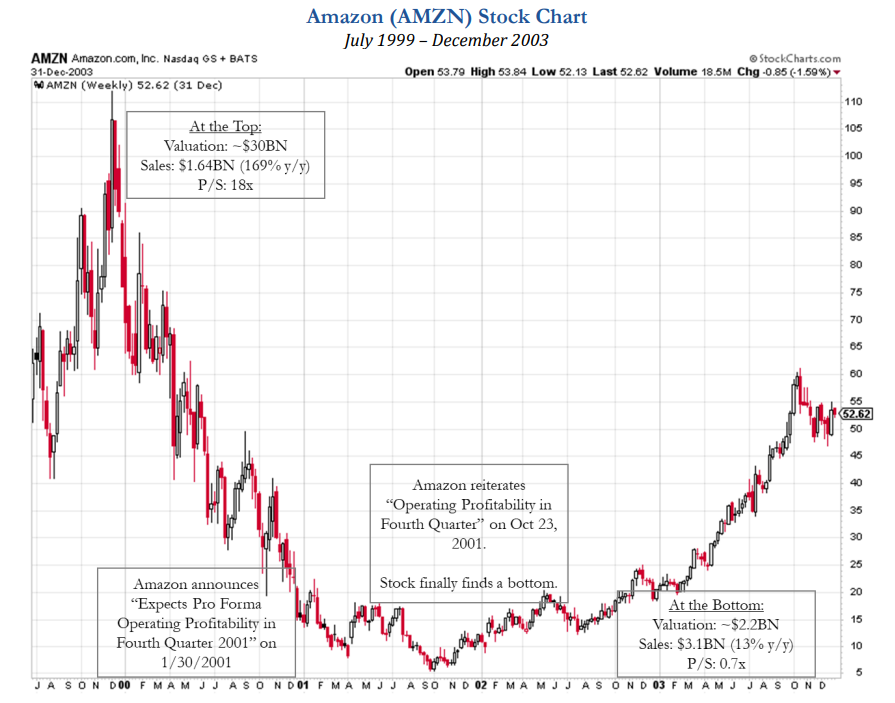

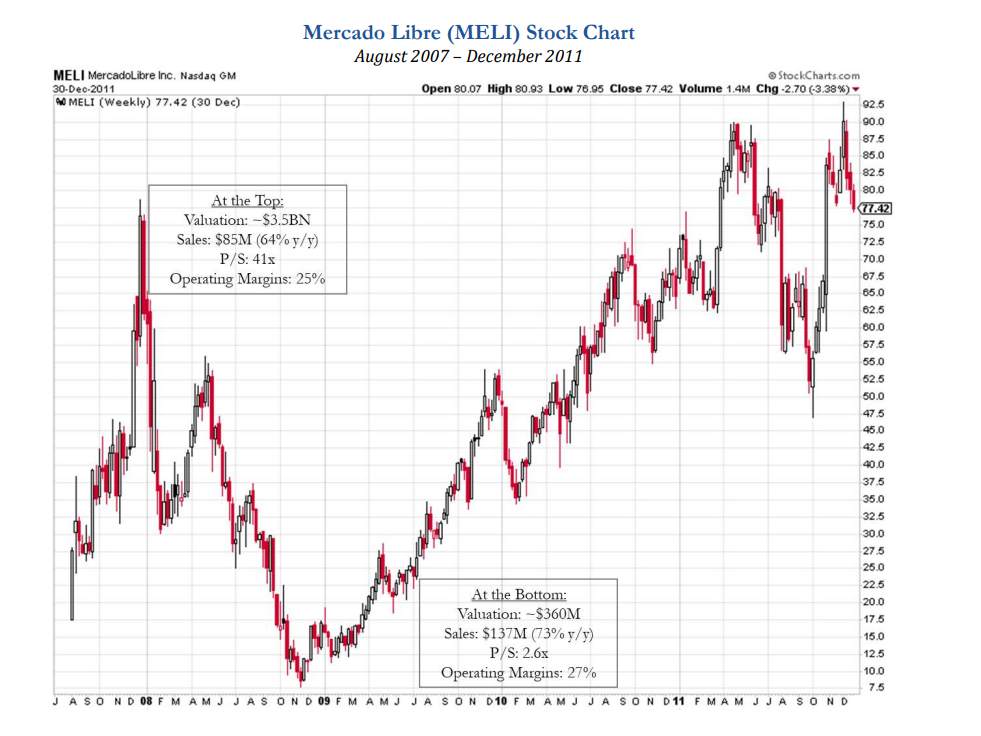

Amazon and Mercado Libre (MELI) Case Study

These two case studies are courtesy of Hayden Capital who studied them during the early stage of their businesses and the drawdown impact that have hit them back in 2000 and 2008.

The first one is Amazon, which is one of the top representatives of the FAANG family which everyone recognizes today.

When Amazon hits a peak by the end of 1999 before the dot com bubble hits at a market cap of $30b, the company was generating a revenue of $1.64b in that year, which is equivalent to a Price to Sales valuation of about 18x at the peak.

Amazon was a 1P retailer back then at the time, so it was still consuming inventory and had to sell it to the retailers. Under this model, operating margin was just at about 5%.

The stock made a historical mouth-watering crash of 93% by the time it bottomed in Sep 2001, and at that time, shares were trading at 0.7x Price to Sales. In the years that the company came crashing down, the company continued to revamp its business model, generate more revenue and increase its operating margin, but capitulation and bear market fear kept investors from holding and buying more, and instead many did the opposite and sold even more.

By the end of 2003, the company has generated $5.2b in revenue, made its first full year of profits and the share price has recovered to 4x P/S valuation. In share price terms, the stock price has returned 850% from the bottom.

Mercado Libre (MELI) was another company that has suffered a drawdown of close to 90% during the great financial crisis in 2008.

For those who were not aware what MELI does, it is an ecommerce company based in Latin America, and following its IPO back in 2007, the share price shot up to a peak in Dec 2007 at a valuation of 41x Price to Sales (the company generated $85m in that year but was valued at $3.5b.

Contrary to its rivals Amazon, MELI was profitable from the time of IPO and was operating at a high margin of 25%, but despite the growth, economic conditions and capital flight left investors to sell out of fear.

The share price retreated to as low as $8 back in Nov 2008 even while revenue increased to $137m. This equates to a valuation of 2.6x Price to Sales and 10x operating profit at the trough. Soon after the worst is over, the share price continues to reverse trend and reached $50 by the end of 2009, providing a return of 525% from the trough at a valuation of 9x P/S.

The rest is history and today MELI is trading at about just over $800.

New Standing Committee of CCP

With the 20th National Party Congress leadership pretty much but all concluded by now, the new leadership team is formed and pretty much aligned with the goals and expectations of the ideology of what Xi is trying to bring to his reign.

Xi’s consolidation of power can mean good or bad as there is now very little opposition that can challenge to what he can or cannot do.

When Xi first came to power back in 2012, only one committee was together with him as an ally. Still, he has managed to reign over the infamous corruption policy which he and his team so effectively guard against, and after the clean-up the companies that were so badly affected reigned stronger after that (just take a look at what companies like Oriental Watch is like after the clean-up).

When Xi was elected for this second term, there was still a balance of power under the previous elected Hu Jin Tao’s League Fraction. In a way, you could say there was balance and check required in a government set-up.

In Xi’s third term, he finally seems to get his consolidation of power and selection of the leadership team that he wants – the market reacted very badly to this, but it can be a double-edged sword.

First, he can now move things faster and reign his ideology with little opposition. This can be seen as good or bad depending on how much effective his policy is or against the wider nation. My sense is that while this may be counter-productive to certain industries, he will still need the assistance of these bigger companies to scale if he wants to achieve both of his two main goals – GDP growth and Common Prosperity for the nation.

For sure, there are certain elements in industries such as EV, Biotechnology, Supply Chain, and Semi-conductors that the country will be particularly focusing on, but for as long as the company you invest in is in a neutral industry, it should benefit them indirectly as an overall measure of the GDP growth.

The political risk surrounding China-US-Taiwan tension is something which has been and will be there for decades, so it is an immeasurable risk that cannot be contained even if say, we have a different president elect for China and the US.

Final Thoughts

My final thought on capitulation is that it can happen to any companies in any sectors in any markets.

As we’ve seen from the example of Amazon and MELI, capitulation can happen when there are severe capital flights out of the market and while we can look back on hindsight, it was never quite obvious, and we do not know it until you and I are a part of it.

To the others who feel uncomfortable investing in China after the new leadership is formed, you should sell or maybe allocate a lesser proportion to account for the risk you would be willing to stomach.

I wouldn’t have expected so many readers to follow me and suffered a capitulation when they have to sell their position yesterday to surrender but if it is, then maybe I will relook at the way how I share my positions in the future in this blog. By no means I was trying to entice anyone to follow me to invest in any companies in any sectors, and I think as adults, we all have accountability to account to ourselves for both our winners and losers in this investment journey.

For those that can survive this (we’ll see what happen in a year’s time or two), it’s probably a good lesson and print and award yourself a bear badge at the end of it.

If you have not followed my social channels, you may want to do so as I frequently post ideas and thoughts in those channels so if you are interested, you may follow me at my Facebook, Instagram or Twitter profile here.

Thanks for your perspective!

Hi Brian,

Just want to let you know im in this journey with you. Have invested $400k+ in Alibaba (50%), Tencent (25%) and 3067 ETF (25%) and still adding.

Thanks Stan, stay strong, we should be rewarded eventually.

Thanks for these insights.

Changing the subject a bit, are you not starting to see value in US tech stocks at this period?

Hi Suresh

Probably a little but not overly, will probably continue to add slowly going into 2023, but with US I still do see macro tailwinds risk still playing out.

Hi Brian,

Baba continued to free fall as of 28 Oct. Whilst I respect your conviction in this counter, I do think its really the end of the road for Ali Baba. I think it could be a $5 stock in 2 years time.

Regards,

Gerald

https://sgwealthbuilder.com

Hi Gerald

Nice, did you pluck that number $5 from your premium article to your members?

Hi, I am curious on your valuation on Alibaba and Tencent. Compared to 5 years ago, the EPS for the 2 has grown by about 5-6% CAGR. In this sense, have you recalibrated the fair value for both companies assuming a base case scenario of 6% growth? Will be interested to know the fair value of both

Hi CC

Not yet, will probably see and do an update once earnings are out soon.