This will be a quick short update as I’ll be away for a short trip getaway next week during the school holiday.

Long story short, I had about $10-$15k of spare cash this month which I wanted to inject into the dividend portfolio. With Jackson Hole being the centre of attention last Friday, this gives me an opportunity to enter into the US REITS listed in SGX earlier this week.

I already had a small position of Elite Commercial REIT in the SG portfolio so naturally I had to look to the US for some high yield play. The US office REIT came to my attention as their share prices were beaten quite dramatically this week as fear of rising interest rate once again comes back to haunt the REITS.

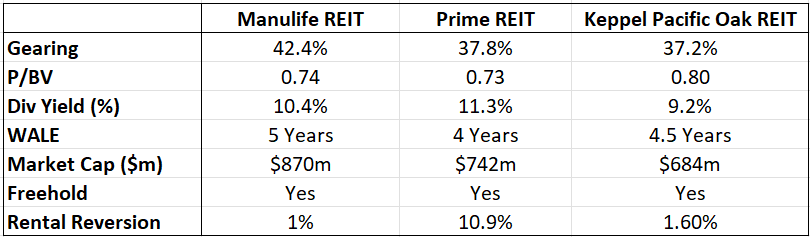

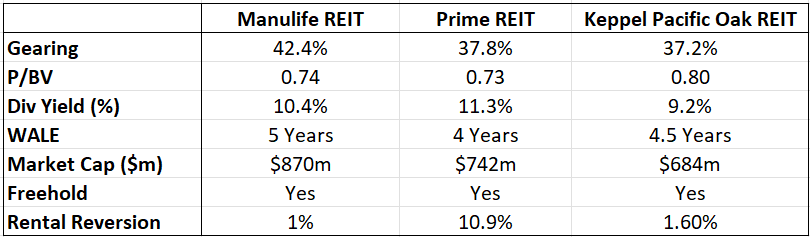

There are 3 office REITs to consider upon – Prime REIT, Manulife US REIT, and Keppel Pacific Oak REIT.

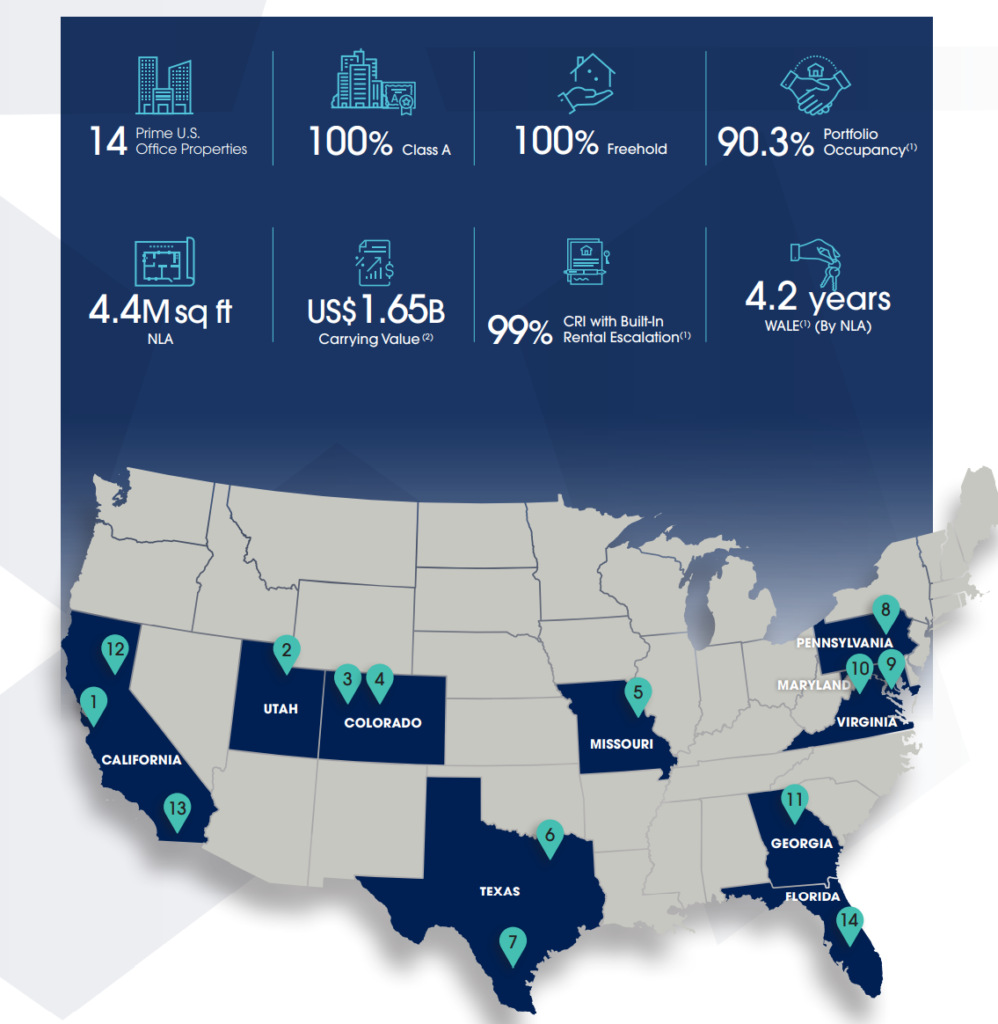

Each of them has their own unique proposition of geographical sectors and properties that they were strong and weak in. To be honest, I didn’t really deep dive too much into this as I was more focused towards the bigger macro play.

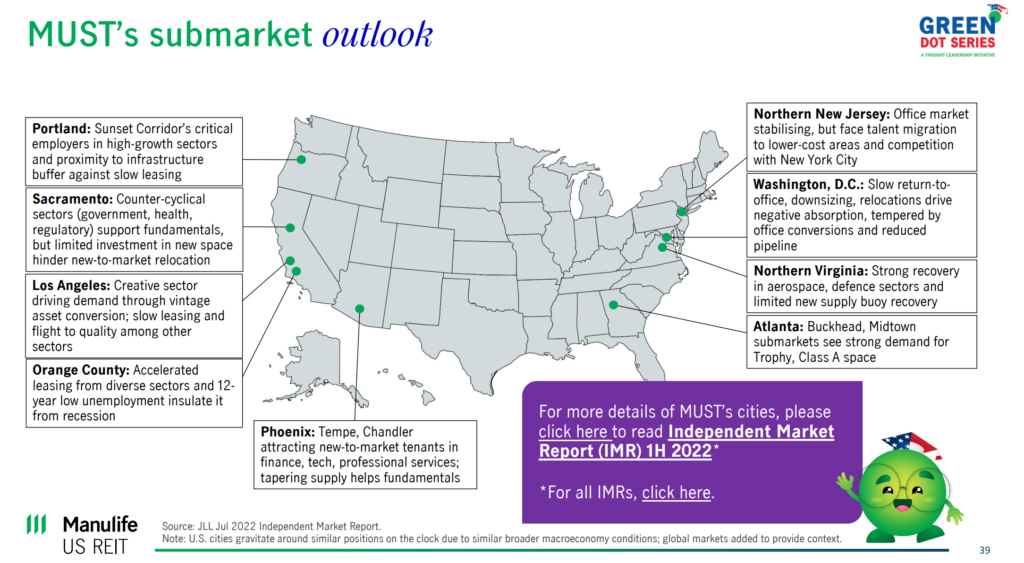

There was one slide in Manulife REIT presentation that 5 major cities where they had their sub-market properties on are in a bottoming phase, and they are expecting it to rise in the next cycle. Still, I am waiting to see a clearer direction from the rental revision from these market.

If we look at the comparisons between one cities with another, there are a few particular upcoming sectors which might benefit more from the sun belt tech areas and higher potential population growth, but most of them are pretty much neck to neck with one another.

You can’t really go wrong with any of these 3 office REITs unless management decides to self-explode by going into different direction completely or destroy shareholder’s value by raising rights at a low valuation.

Either way, the properties and assets are freehold and full of quality in nature, so it’ll be a matter of time before we get a payback breakeven in terms of the investment.

I kept thinking if higher inflation and rising interest costs will be a factor but these rising operational costs come with higher rental reversion negotiation on the table so there are rooms to stomach for this risk.

The only worry is the structural office directional play in the future, whether this will be a relevant thesis in the future as most companies are on hybrid working. We can continue to monitor this from the leasing occupancy as well as the rental reversion from each property.

At the end, I decided to go with leasing and rental reversion momentum and ended by purchasing 16,000 shares of PRIME REIT this week after all considerations but I will probably limit my threshold to office REITs at this range threshold.

If you have not followed my social channels, you may want to do so as I frequently post ideas and thoughts in those channels so if you are interested, you may follow me at my Facebook, Instagram or Twitter profile here.

Dear Brian

Thanks

I hold all the three and to be honest, regret my decision. Overall, all three have caused significant capital erosion that is unlikely to be reversed even if , miraculously, the physical occupancy picks up with positive rental reversions. The current dividend yields are tempting, no doubt, but might get cut significantly if rates stay high

Unlike Singapore and the East, the management can not enforce physical attendance as the westerners would not only threaten to quit but more importantly can also sue for harassment !

I am very skeptical about the prospects for these three. Plus, Sg investors recently have been shunning REITS with overseas holdings and prefer to invest in “what they know, can see and feel”, rather than overseas REITS

The interest rate hikes are unlikely to go down fast and until then the suffering will continue

I predict MUST, KORE and PRIME at 45, 60, 57/58 cents very soon

Happy to be proven wrong but I got to be realistic

Best wishes

Garudadri

Hi Garudadri

Thanks for your views.

To be fair, they are not the only one suffering from the higher inflationary and risk environment. Most of the US and global companies are suffering this year due to the same theme. Most growth oriented companies in the US got it worse than others. While these office REITs have performed poorly as compared to the local REITs, I feel like they should have been compared against some of the other US companies.

Your target for each of these individual REITs aren’t that far from today’s price. Most of these targets are within a year of dividend for these REITs which is a beauty of REITs these days being able to surface higher payout. If my average price for Prime is 63 cents for instance, a 6 cents dividend would mean my average cost would drop to 57 cents next year, and then 51 cents the following year. Sure, we do not know if the situation is going to get worse and if they will cut dividend, but the idea of the dividend is there. When the US economy recovers and gets better, I hope they will still be relevant by then, and share price would follow.

Hi Garudadri, I agree with your view 90%. there is a chance it can get lower. but it does get to 58, I will scoop some 🙂