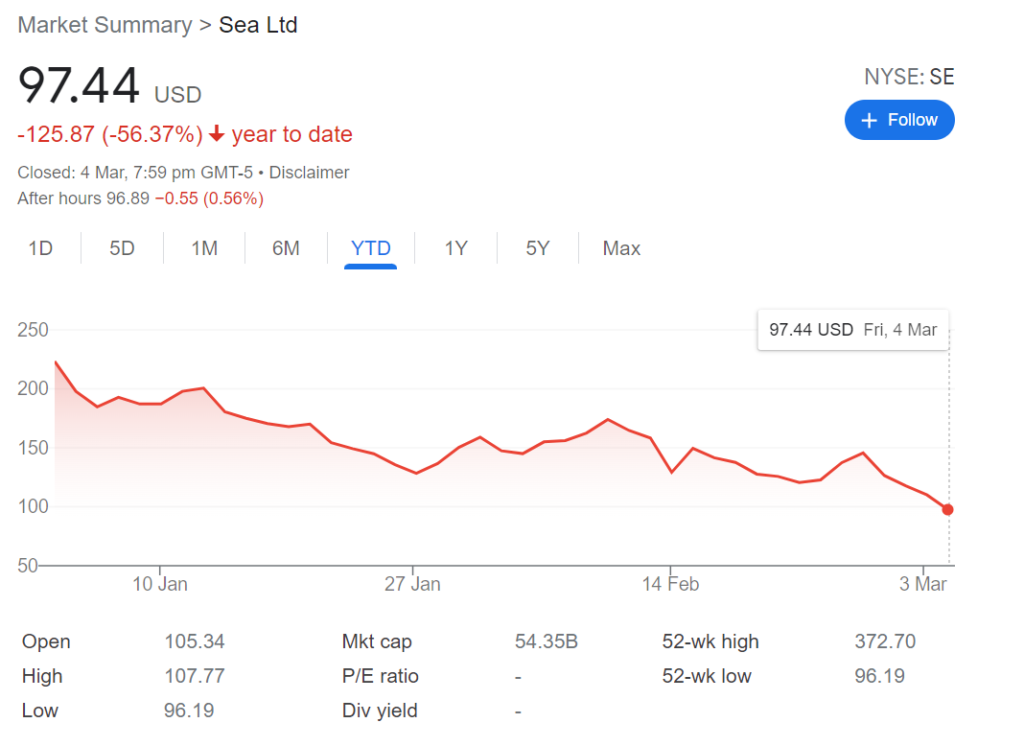

On Feb 7 this year – right about 3 weeks before the announcement of their Q4 results – I posted an article about shorting Sea Ltd at the range of about $160ish, which is at their top end of the resistance line.

Since then, the company has gone sideways in terms of the share price until the recent announcement of the Q4 results which sends the company plunging down to below $100 at yesterday’s closing.

It has since lost about 74% of its market cap since it last hit a peak of $372 on 19th Oct 2021 and it has lost about 40% since the announcement of the results just this week alone.

When Micro & Macro Headwinds Combo Hits,

It Is A Perfect Storm

There were signs during Q3 that Garena was slowing down in terms of sequential growth quarter to quarter. So investors shouldn’t expect a miracle otherwise that Garena was going to reverse that in Q4.

Garena’s Free Fire – which has been a cash cow for the company for a long time to fund its e-commerce and fintech business, also guided for a slower revenue in 2022 YoY, so that comes with a huge punishment for investors that value SEA Ltd as a growth company.

Management guided Garena bookings to decline to ~$3B mark in FY22, which is a reduction from $4.6B in FY21. This is attributed to the normalization of bookings post-Covid (which usually will come at some point for most companies) and also a banning issue from the recent India regulators on Free Fire.

Speaking of the India commissioner regulators, the commissioner has closed recent case filed for Shopee India against anti-competition due to it’s low pricing power that puts smaller enterprise out of business. You can find the full details here.

At least we now know the worst from the Free Fire and Shopee India has been priced in.

Other Macro Factors leading to inflation, rising rates and conflict war between Ukraine-Russia didn’t help the cause either for the stock market (at least in the short term).

When you have all these added up, it makes a perfect storm warrant for market decline.

Why I Think Sea Ltd At $100 Is Relatively A Good Deal

As investors, the hardest part about finding a decent entry price and being vested when market is bearish is to actually take action and get in.

The market will always price in the fact that it will continue to go up even when it feels so expensive, and it will push price down lower when it feels like it is already cheap.

Ultimately, it is about balance between the two and which prevails giving longer term returns for you.

In my Facebook page last night, I have announced that Sea may have a psychological support at $100 and why I have decided to turn my shorts to long at $100. Clearly, this support doesn’t hold and I am now slightly underwater but I’ll explain why I think it’s still a good deal.

We can take a few approach of how we want to look at this several ways.

Comparison Metrics:

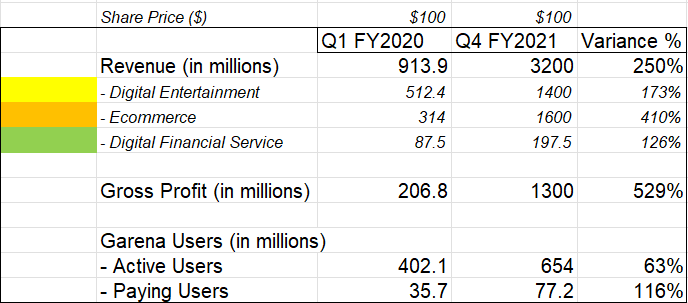

The first is a comparison across the unit metrics back when Sea was also trading at this same range ~ $100 – which was back in May 2020 right when Covid was still heavily rampant throughout.

Back then when they reported their Q1 FY2020 results, the company still look relatively small base and they were about to reach their first $1b revenue.

Garena was only reporting at $512m, Shopee at $314m and Sea Money at $87m.

Fast forward a couple of quarters later (7 quarters to be exact), Sea is today reporting $3.2b in total revenue will all metrics up triple digit in the right direction.

I guess what I am trying to say here is that the market may have been overly focused on Garena’s slowdown guidance and if you like the valuation at $100 back then, you should like it even more today with metrics significantly better and stronger.

Sum-of-the Parts:

The other methods we can use is to break it down into sum of their different parts.

The easiest to chop from the parts is their net cash and cash equivalent less debts, which is today standing in at ~ $9.5b. At the current share price, this represents about $17 of their entire market cap today of $54b.

We can argue that the company is still burning cash at the moment and the burn-rate over the next few quarters might deplete this amount further. I’ll leave that to how conservative you want to come up with the scenario.

Garena’s is profit making – and in Q4 they booked in a total of $602.6m of EBITDA bottomline. For full year, the division is making $2.78b of EBITDA profits. If we assign a reasonable amount of enterprise value for this division at 8x multiple, we would get ~ $23b thereabout.

E-commerce Sea platform is still burning at a rate of $2.55b for FY2021 but have guided for positive adjusted EBITDA in South East Asia and Taiwan by 2022 and a positive overall EBITDA for the division by 2025 so at this moment, we can only depend on the Price to Sales revenue guidance to make our case.

E-commerce revenue guidance forward for FY22 is at ~$9b, so if we assign a conservatively 3x P/S (which I think is rather low), it will give us $27b. Once Shopee gets to positive EBITDA, we will look again at the margin and how much multiple they can fetch from their bottomline.

Digital Finance Service – Sea Money is still in the early stage so there will be room for growth in this segment for years to come. Prescribing a higher Price to Sales multiple (but still conservative) at 5x for this segment on FY22 guidance, we get a $6b worth of enterprise value or $11/share.

Totalling everything, we get a runway of about $118 worth of intrinsic value of what you are paying today for what I consider to be a conservative multiple. Given management’s execution and capital allocating ability in the past, this should relatively be a walk in the park, even if they are late going into profitability a quarter or two for the other two segments.

Baba to me feels like the cheaper play of the two if you want exposure in this sector but with the market punishing these companies so hard, I think this makes a good longer term play for those who are willing to ride the storm.

Hi Brian, your China/HK tech stocks are so underwater now and with the Russian Invasion, I foresee relations between the West and China are going to get more confrontational (not good for China’s economy). What are your plans to ride out of this situation? keep selling call options to bring your average price down? but when prices are so underwater, how much can you make from selling calls? Would be interesting to hear your views.

* I do have some HSTECH etfs and they are a disaster. Thankfully I don’t hold much.

Hi James

It is unfortunate that the war is happening but the best course is staying put to the cause with macro-economic factors leading the swing in the market. China/HK tech stocks are not the only sole cause of victims, if we look across most tech stocks in the US outside the big few ones, a lot are in deep trouble territory. I guess it is important to relook at the thesis again and not let the war situation plays out and impact your decisions to sell out of fear. As long as we have a longer duration of expectation, the war (like any other wars and Covid) will eventually subside and the world will move on from there.

Selling calls is probably not the best time to do so right now as it caps your upside should things turnaround quickly and the premium is not the best reward in current environment.

Hope this helps.

I have no doubt the US tech stocks -those making profits and generating positive free cash flow- would rebound after the war.

but do you think the China/HK stocks you are holding now are permanently impaired given the political situation in China and outside China? I suspect things would not be business as usual in China (common prosperity, more internal self-reliance, moderate economic growth rate) and outside China (I believe the West would be more hawkish towards China even after the war). You have so much capital tied up in these stocks that may or may not recover.

Is it time to revert back to the Brian Halim of the old and start investing in quality dividend generating stocks (many of which are holding up pretty decently for now)

Hi James

I do not think the business in China is permanently impaired. I’ve covered grounds on my thoughts on common prosperity and in my view it is for the overall good of the economy which would trickle down ultimately to GDP expansion for the country itself. The benefits may not be tangible by individual companies right now but in the longer run it would.

Also, I appreciate your comments but I think you should stop thinking about what you think I should be investing in and worry about your own positions. A debate on certain factors is okay but it is not okay trying to suggest some things to somebody whom you barely know about. Thanks!

Peace 🙂

Apologies James if I sound rude earlier. My intention was never to inflict conflict in this environment. Clearly the investment has not worked out well so far as expected and this applies not to myself but for everyone involved who is invested in US tech and Chinese stocks in general. I’ll give your suggestion another thought.

Hi Brian,

I have been following your blog for a long time and I felt that James made a good point. Why are you so triggered? Did these bad calls get into you?

P.s Not here to start a keyboard war. Peace.

Hi Jalan

I felt like it is okay going into debate about specific topics but the part which I am not okay with is suggesting someone to use a certain practice where our circumstances are different. For instance, it wouldn’t be nice if I start asking you or James about why didn’t you guys go full fledge into China or tech when they are at the bull. Maybe I read it a bit too sensitively, but let’s just keep that debate about growth vs dividend investing separate.

Over the years, my investing has evolved, partly due to the fact that I am now working in a tech industry where my knowledge on this sector evolves. I don’t think we could comment about anyone whether growth or dividend investing is the right method of investing for someone when the timeframe we are looking at may be short in nature. But that is my opinion. He may be right at the end of the day but I don’t think it’s nice to put it down like that. I have also apologised to him in my earlier comments as I may sound a bit on the rude side. Peace.

Hey Brian,

Thanks for the summary here, your honesty with positions on top of your views is much appreciated.

With regards to the naysayers, I do concur that it is slightly rude to recommend that another person do something differently, especially saying something is ‘good old’. Nobody is right all the time, and claiming another asset is ‘good’ at the time when the other underperforms is simply cherry-picking rather than sound advice.

Stay strong everyone

Hi Karina

Thank you for your kind words.

No worries, it is a misunderstanding and probably I am reading it a bit sensitively from my side but I think we are all good and it is important to just have that slight faith lights up when things are at their worst.

Take care and stay strong too.

Noted Brian. That makes sense, thanks for replying. 🙂

Hi Brian,

No worries, no offence taken here :). I like abit of passion in discussions haha.

My personal view is that regardless of how markets are doing, it is prudent to hold a diversified portfolio (geographically, industry and types e.g. some growth and some value). I’m just puzzled with your very heavy weightage in China Tech.

It was another horrid day for Chinese Tech stock yesterday. Hope things stabilise soon. But we should also count our blessings that we are not suffering like the Russians and Ukrainians.

James

Hi James

Glad we thrashed out that misunderstanding 🙂

I guess on hindsight I shouldn’t have taken such a heavy weightage and am now paying the price for it haven’t I? Haha… The thought process behind it was nothing looks cheap last year other than this particular sector so the addition keeps to be revolving around the same piece. I guess I was expecting it to be that bad, but not expecting it to be THAT bad. In any case, it is probably a tad too late to rotate right now so I’ll just keep that faith going for now.

Meanwhile, given the US has corrected too recently, I have added some solid positions to diversify as well (they are underwater right now) and we’ll see how it turns out over the next few years. I’ll provide in my monthly portfolio updates for this month when it is ready.

But other than that, you are right – we count our blessings to be able to live our normal lives undisrupted, eat and sleep well, vacation on the cards (finally cruise for my family next week!) and a good job to tide over. Can’t complain much.

Thanks Brian,

I must say I respect your transparency and openness is sharing your positions (the wins and the ahem). I can’t say the same for many of the other Financial Bloggers out there. Sometime we don’t know if they are putting money where their mouths are.

Enjoy ur holiday 🙂

James