Most new investors step into the stock market learning through the fundamental series of the company.

Don’t get me wrong – understanding the basic function of how a business works in the real world and how they are being valued is very important in investing but they are just half a battle won.

Most people spend time focusing on the hard technical part of investing but forget there’s another element that’s worth paying attention for – The Execution.

For instance, an investor might have excellent analysis skills and is able to develop a financial model to value the intrinsic value of the company but when it comes to the real war, he might drop out in the trust and confidence of the model he once built and might not be able to execute his plan as well as he should.

In the complex world of uncertainty, many falls under the tendency of hindsight bias knowing that certain things look so much easier on hindsight than being present on the day itself.

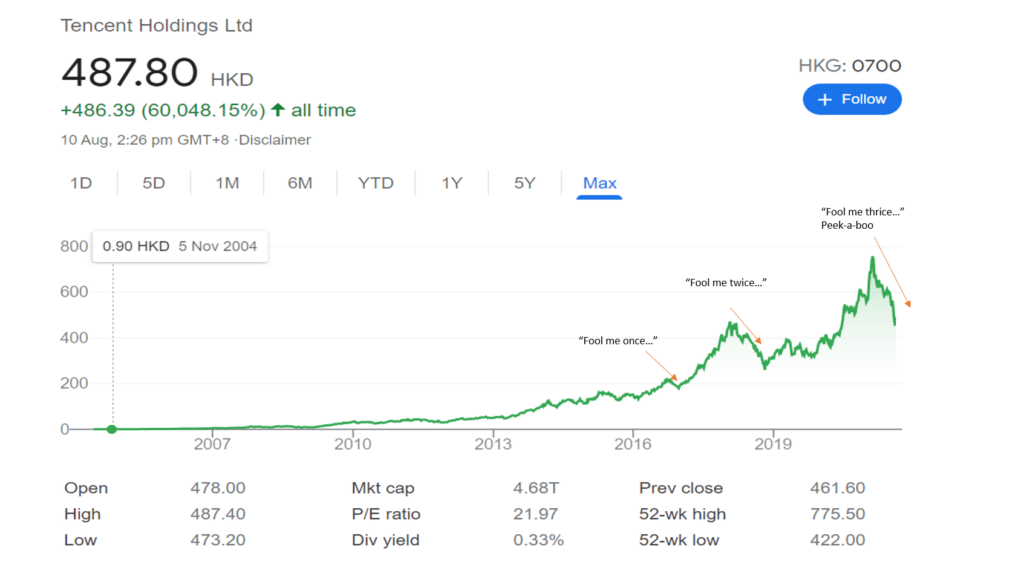

Taking a step back looking into the Great Financial Crisis of 2008 and the last COVID crisis back in 2020, there were many who were calling for the end of the world and that the stock market would crash like no one seen it before. The proceeding articulation of bad news one after another came through the spotlight of the media, giving further doubts to naysayers who think it’s “better to wait a while until things are more stable”.

The Elements of a Strong Executor

A Strong Executor is someone who uses all the information, knowledge and experience he has accumulated through the years and have the conviction to make the right call.

A study conducted by Harvard Business Review underlines the 4 most important traits for a strong executor.

These are the Information, Decision Rights, Motivators and Structure.

Information

Information is important because it helps us to remember details and gather thoughts which would be important in our decision making process later on.

In a battle of war, these are your critical resources to knowing each and every information you have regarding the enemy – whether it’s the number of armies, the effectiveness of weapons, the conditions of the wind, etc.

For an investor, these are your technical hard skills that you have been focusing and honing over the past few years – learning about the business moat of the company, understanding the financial statement, getting to know the management and leaders of the company, building the financial model for valuing the company and so on.

A good investor would be able to differentiate between what is key information and what is noise, as information tends to flow easily these days through the ubiquitous prevalent use of media.

Motivators

Motivators is an investor’s performance commitments.

We have to be clear of what we want to achieve investing in the stock market and the performance commitment needs to be something that is quantifiable in nature.

For instance, if your goal as an investor is to earn a decent 5% per annum in the market out there, then it would make sense to allocate your portfolio based on different asset classes that would act as a “stabilizer” to the entire portfolio. One reason for this is because the long term return for S&P alone is roughly ~10% so that would act inevitably as a benchmark if you are trying to do stock picking against the index. It would also not make sense if you are trying to achieve 5% return and then have the most part of your portfolio invested in volatile meme stocks such as GME or AMC.

Conversely, if your goal is to earn say a long term 25% per annum through premium stock picking, you would have to be bolder enough to invest in compounders and taking part objectively in a correction or bear market setting.

Structure

By design, this would reflects the capital structure of an organization which obliged each slice of the stack and resources that’s available to the company.

For large corporations, this would typically consists of the senior debt, subordinate debt, hybrid securities, preferred equity and lastly common equity.

For an individual investor, having a structure would reflect the current conditions of having your investment not connected to any of your other obligation in life. In other words, this should be funds that you are willing to risk in the market and should not impact how you live your life outside investing no matter what the outcome is in the market.

For example, if you are taking $100,000 of funds out to invest in the market, knowing that you may need the money a year or two later to get married and buy a house – this may lead to indecision or executing hesitantly which might affect your decision making process as an executor.

The general rule still applies – separate your emergency funds, get your day to day fund needs in order and invest the rest.

Decision Rights

All of the above leads us to decision rights – which is an investor’s level of conviction investing in that particular stock or market.

Conviction is not something which an investor can learn overnight as it is still very much depends on many factors influencing the comfortability of that investor’s willingly taken risk appetite.

It is a firmly held belief and a risk worth taking after all the considerations of the different traits have been considered and well balanced.

Having a conviction is not just about putting large amount of money in one investment (that’s another topic for another time) but is particularly important in a hard setting environment.

For instance, the unsuccessful tenure for Joseph Schooling in his 100m butterfly event is a particularly hard one to swallow because many of us were expecting more to come from him (even I think he himself is expecting better outcome from his favourite pet event).

In the stock market world, there is no one single correction and bear market that looks easy for an investor to swallow.

During a correction or bear market, there will be a plethora of bad news one after another with the media trying to sensationalize the events to make it a headliner. Worse, we would also have management that guided very cautiously of their upcoming earnings, perceiving the outlook as grey and tough environment to operate in.

There will be drawdowns in most investor’s portfolio – drawing blood in between 10% to 60% each time depending on the severity of the crash. In this situation, the true calling will draw upon an investor’s mettle and mindset, testing who is ready to face such a turbulence.

Conclusion

Over the years, executing is one trait which I’ve been trying to improve upon as an investor myself.

I’ve made decisions that gone wrong – either having sold my winners too fast or my losers too slow.

I’ve experienced the cold feet during a bear market when my portfolio was down by over mid 5-digit in a single day while I am trying to navigate my way through the supermarket alley, considering which of these apples are cheaper to buy from.

I’ve drawn blood – not to the extent where I have to surrender overnight but is enough to give me sleepless night – either in excitement anticipation or in anxiety.

I’m definitely far from being a perfect executor, but all the experiences and learning are one thing which I’ve taken in stride.

Executing is something which I think is very much underappreciated in today’s environment but is something which can be incredibly important to take note of.

The art of execution is more than just an expression form – it is a combination of all the elements that we as investors have honed together.